No 6502

Wednesday 18 April 2018

Vol cxlviii No 26

pp. 496–524

The Council begs leave to report to the University as follows:

1. Further to Regent House approval on 18 February 2011, the University issued a public bond for £350m on 17 October 2012 at a fixed interest rate of 3.75% (Reporter, 6213, 2010–11, p. 490; 6280, 2012–13, p. 35). The bond, with proceeds now fully utilized on Phase 1 of North West Cambridge, falls due for repayment in 2052.

2. In March 2015, Regent House approval was given in principle for further borrowings of up to £300m for income-generating projects, should the business opportunities be confirmed and borrowing conditions remain favourable. This authority was renewed in 2017 for a further two years to May 2019.

3. For reasons described below, the Council is now seeking to raise the authority to arrange further external finance from £300m up to a total of £600m.

4. With very low interest rates currently available, by investing the proceeds of borrowing in projects that produce revenue, the intention is to generate, over time, a net surplus. Any net surplus would then be available to support the core strategic mission of the University, benefiting the organization over future generations.

5. While additional external borrowings would increase the University’s total long-term balance sheet debt, the Council does not consider that external borrowings at the levels considered in this Report would have an impact on the University’s ability to fund any increase to employer pension contributions within the ranges under discussion in the context of USS (for example, were Rule 76.4 to be triggered, employer contributions would rise from 18% to 24.11%).

6. The University has historically funded its capital programme for the academic operational estate through a combination of external government grants, philanthropy, and receipts from Cambridge Assessment and Cambridge University Press. As the University continues to embark on an extended period of intense strategic capital development, affecting most of its principal sites, the Capital Plan, under the management of the Planning and Resources Committee, projects the likely capital aspirations of the University over a 20-year horizon to be some £4bn. This is an ambitious and financially demanding programme, particularly given the loss of capital grants from the government. Philanthropy must play its part through the coming campaign, and receipts from Cambridge Assessment and Cambridge University Press will continue for the present to be channelled into the Capital Fund.

7. However, these funds are insufficient in themselves to support capital developments for the operational estate. For that part of the University’s estate, therefore, the Planning and Resources Committee is undertaking a more robust prioritization of the University’s operational capital building programme.

8. In parallel, there is also a requirement to continue to invest in our non-operational capital estate in order to support the University’s long-term strategic objectives. Developments that generate income, with which the interest and principal of any borrowed funds could be repaid, while also generating a long-term alternative income stream to support the University’s core mission and student interest, are attractive opportunities and it is in these areas where borrowed funds would be applied.

9. New external finance would thus directly benefit important non-operational estate projects which provide tangible, long-term return of financial and strategic value to the University. In particular, it is envisaged that a significant proportion of the proceeds would be targeted towards the critical provision of further housing solutions.

10. The Council continues to consider the most appropriate approach to the governance, oversight, and operational management of the growing portfolio of non-operational estate, including the involvement of appropriate external specialist advisers.

11. The University has a number of income-generating proposals at varying levels of maturity, which collectively indicate a demand well in excess of £600m. These projects all have the potential to deliver commercial risk-adjusted returns. While the targeted use of proceeds from the financing would not be specified in the external documentation, it is anticipated that a significant proportion (currently forecast at £300m–£400m) would be invested in North West Cambridge Phase 2 if approved (in early 2019). If the second phase of this development were not to be approved, it is anticipated that a similar level of funding would be required for alternative projects to meet the essential need for further housing, especially for key workers.

12. Additional income-generating projects are likely to include further rental or shared ownership housing to meet needs not fully addressed by North West Cambridge, the redevelopment of the Royal Cambridge Hotel, commercial development of the old Cambridge Assessment buildings and the Old Press Mill Lane site, the commercial research development strategy at West and North West Cambridge, and projects targeting environmental benefits, provided adequate risk-adjusted returns are met.

13. Over the period since the University’s 2012 public bond issue, interest rates have continued to fall and the spread to underlying gilts has narrowed. The 2012 bond is currently yielding less than 3%. Significantly, pension fund reform has led to increasing demand for long-dated assets and the market continues to demonstrate historically low long-dated gilt yields. The current strength of the Sterling debt capital markets can be seen in the advent of bonds with a 100-year maturity, catering to a demand from investors of highly rated, ultra-long debt issues.

14. There remains strong demand for fixed-rate senior bonds, repayable at maturity (the same format as the University’s 2012 bond), with a current optimum interest (coupon) rate achievable for terms (tenors) of 50–60 years.

15. The Council recommends that the University also consider a proportion (no more than half of new borrowings) of inflation-linked bonds, reflecting the immature, but rapidly developing market demand for such investments. Amortising CPI-linked bonds (under which the principal is progressively paid back over time) of similar tenor to the fixed-rate bonds above, have near-zero current coupon rates, with the potential to reduce the aggregate interest rates of the combined borrowings materially. While it should be noted that the interest and principal repayments of CPI-linked bonds would increase each year by CPI inflation, given the likely linkage of project income streams (e.g. property rentals) to CPI, there would be a natural internal hedge.

16. A combination of both fixed-rate and CPI-linked borrowings would also provide a hedge against long-term high or low inflation outcomes, respectively. A floor and cap would be included in the CPI-linked element to remove University exposures to large variations in inflation outcomes.

17. The Council takes the view that there is now a case for further borrowing and that the favourable market conditions, which are attractive on a historic basis, are unlikely to persist. There remains a need for new finance, directly to benefit projects for which there is a tangible long-term return of financial value to the University and indirectly to support academic capital projects by relieving pressure on the University’s cash flows required for operational capital expenditure.

18. It was vital to the efficient and professional issue of the 2012 public bond that the Regent House delegated power to the Council for a defined, renewable period, on the advice of its Finance Committee, to take forward plans for borrowing against a maximum total value. There are various sources of external finance that the University could seek and factors of cost, flexibility, tenor, risk, and affordability, which the Finance Committee would consider. Any proposals would be in the context of the current financial constraints, risks, and challenging outlook. The process of negotiation with potential lenders is complex and confidential. The Council, with the advice of the Finance Committee, wishes to have the flexibility to move swiftly to secure external finance while market conditions are attractive or in circumstances when conditions could move adversely. As a consequence, the Council is seeking similar powers from the Regent House as those approved by Grace in 2015 to determine whether, when, and how much to borrow, and by what instrument. If the recommendations of this Report are approved, at its meeting in May 2018 the Council will be asked whether it wishes to issue a bond and, if it does, to agree the parameters for its issue. If the Council is content, a sub-committee of the Finance Committee, acting under delegated authority, will determine whether the conditions are right to act on that approval.

19. Additional external borrowings of £600m would increase the University’s total long-term balance sheet debt to £946m or 19.5% of net assets.

20. For clarity, the Council wishes to confirm that the authority for advancing external borrowings sought in this Report would not have an impact on normal University governance processes for seeking the approval of individual development projects.

21. The Council recommends:

I. That the Council be given authority in advance to arrange, on the advice of the Finance Committee, external finance for income-generating projects up to a total additional amount of £600m, potentially including an element of CPI-linked borrowings with the advantages and risks noted above.

II. That the higher limit of authority will apply for the remainder of the existing period of authority to May 2019. To the extent that this authority is not fully used, the Council would request continuation of the authority on a rolling two-year basis annually by Grace.

|

18 April 2018 |

Stephen Toope, Vice-Chancellor |

David Greenaway |

John Shakeshaft |

Richard Anthony |

Jennifer Hirst |

Sara Weller |

|

|

Stephen J. Cowley |

Fiona Karet |

Mark Wormald |

|

Daisy Eyre |

Mark Lewisohn |

Jocelyn Wyburd |

|

|

Anthony Freeling |

Susan Oosthuizen |

||

|

Nicholas Gay |

Michael Proctor |

We have yet to see a sufficiently clear business case with enough detail on the funding model and how repayments for a new bond will be achieved. We should not risk our AAA rating and put the next generation in this sort of debt until we have clarified more of the detail. The University’s record on the first phase of North West Cambridge does not inspire confidence; the development was two years late and £100m over budget. Work continues to update the existing rental model to ensure that the current bond liabilities are fully covered in the expected timescale so that there will be no further calls on the Chest. As Trustees we should insist on greater financial and procedural clarity surrounding a second bond before proceeding.

|

18 April 2018 |

Ross Anderson |

R. Charles |

The Council begs leave to report to the University as follows:

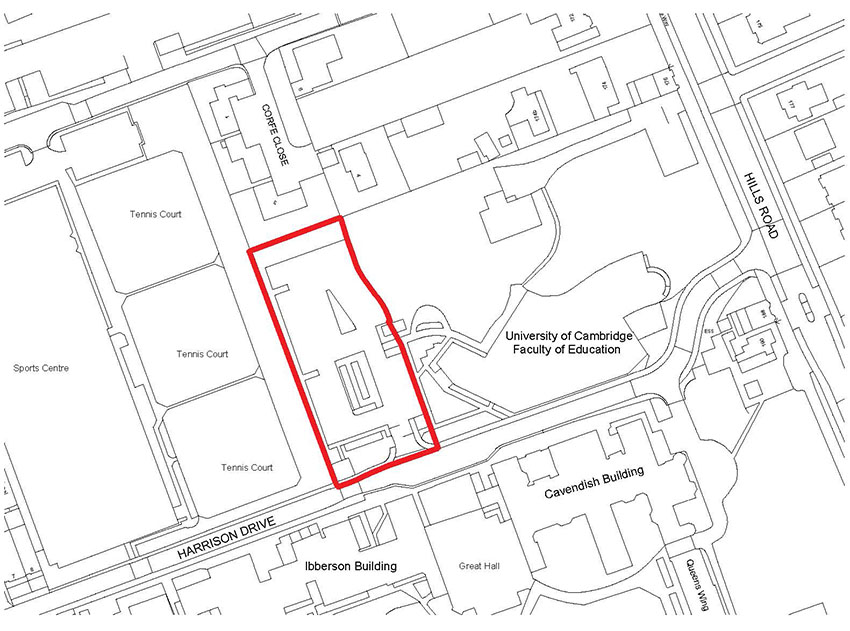

1. This Report is seeking approval for a new nursery building on Harrison Drive, off Hills Road. The nursery would be built on land leased from Homerton College over a 99-year term which commenced in January 2005; the space is currently being used as a car park by the Faculty of Education. Car parking for the Faculty elsewhere on the Homerton site is under discussion with the College.

2. The expansion of existing nursery services is a priority for the University and regarded as critical to the recruitment and retention of staff. The new building would provide an additional 100 spaces for children of staff and students, and would make a significant contribution to reducing the current waiting list, which far exceeds existing capacity.

3. The new building shown in the accompanying plan would be constructed in a single phase at an estimated cost of £3.1m, and would provide a total gross internal area of 620m2. Once the design has achieved RIBA Stage 3, the intention is for the proposal to be tendered to a nursery provider/developer for both build and provision of services. The project will be undertaken at cost to the nursery provider in return for a lease to occupy the building and provide nursery services to the University.

4. The University has not previously undertaken a project with this financial model, and it has been agreed that it will be managed under the Capital Projects Process but with additional approvals sought from the Finance Committee at stages throughout that process. The overall outline proposal was approved by the Finance Committee at its meeting on 7 June 2017. A Concept Case for the project was approved by the Planning and Resources Committee (PRC) on 13 December 2017. Before the project is implemented, it will require a Full Case to be considered and approved by the PRC, and to have final approval from the Finance Committee.

5. A site plan is shown below. Drawings of the proposed building are displayed for the information of the University in the Schools Arcade, and are reproduced online at http://www.admin.cam.ac.uk/cam-only/offices/planning/building/plans_and_drawings/.

6. The Council recommends:

I. That approval be given for the construction of a new University nursery building as described in this Report.

II. That the Director of Estate Strategy be authorized to apply for detailed planning permission in due course.

|

18 April 2018 |

Stephen Toope, Vice-Chancellor |

David Greenaway |

Susan Oosthuizen |

|

Richard Anthony |

Jennifer Hirst |

Michael Proctor |

|

|

R. Charles |

Alice Hutchings |

John Shakeshaft |

|

|

Daisy Eyre |

Darshana Joshi |

Sara Weller |

|

|

Anthony Freeling |

Fiona Karet |

Mark Wormald |

|

|

Nicholas Gay |

Mark Lewisohn |

Jocelyn Wyburd |

Site plan of the proposed new nursery building