No 6773

Thursday 27 February 2025

Vol clv No 22

pp. 288–393

The consolidated financial statements provide an overview of the finances and operations of the University Group (the ‘Group’) covering:

•the teaching and research activities of the University (the ‘Academic University’) and its subsidiary companies;

•Cambridge University Press & Assessment (the ‘Press & Assessment’) and its subsidiary companies, joint ventures, and associates;

•The Cambridge University Endowment Fund (‘CUEF’), the investment fund managed by the Group and holding the majority of the Group’s investments together with some investments of Colleges and other associated bodies; and

•the Gates Cambridge Trust and the Cambridge Commonwealth, European and International Trust (the ‘Associated Trusts’), and other subsidiaries of the Group not included in other segments that undertake activities, which, for legal or commercial reasons, are more appropriately carried out by limited companies.

Further detailed information about the finances and operations of the Press & Assessment is given in the published annual reports of that entity. The Press & Assessment is a constituent part of the corporation known as the Chancellor, Masters and Scholars of the University of Cambridge. The Press & Assessment’s primary work is the conduct and administration of examinations in schools and for persons who are not members of the University, and operation of the University’s publishing house, dedicated to publishing for the advancement of learning, knowledge, and research worldwide.

The Associated Trusts are separately constituted charities. They are deemed to be subsidiary undertakings of the University since the University appoints the majority of the trustees for each Trust. The purpose of these Trusts is to support the University by enabling persons from both within and outside the United Kingdom to benefit from education at the University through the provision of scholarships and grants.

The financial statements should be read in conjunction with the Annual Report of the Council and the Annual Report of the General Board to the Council for the 2023–24 academic year (Reporter, 6762, 2024–25, p. 152). References to the University reflect the teaching and research activities of the University (excluding subsidiary companies and Associated Trusts), together with the Press & Assessment (but excluding their subsidiary companies, joint ventures, and associates). References to the Group reflect the teaching and research activities of the University together with the Press & Assessment, including all subsidiary companies, Associated Trusts, joint ventures, and associates (see Note 37).

The financial position of the core teaching and research activities of the Academic University may be seen more clearly in the Financial Management Information published in the Cambridge University Reporter (see https://www.governance.cam.ac.uk/committees/finance-committee/Pages/FMI.aspx). The Group considers the best measure of underlying recurrent operating performance to be the adjusted operating surplus/(deficit) for the year shown in Appendix 1 (p. 377).The Group defines this as Reported Surplus less gains or losses on revaluation of investments, fair value adjustment for the CPI-linked bond, change in USS deficit recovery provision, donations, endowments and capital grant income, and adding the CUEF income on a distribution basis. This adjusted measure provides a meaningful, consistent measure of the Group’s performance.

The current year has seen a continued increase in activity levels across the Group, albeit that the path of growth has continued to vary across the Group’s large number of different activities. Overall revenues have increased by 4% during the year, substantially driven by continued increases in the Press & Assessment activity, unregulated tuition fees, increased donations and endowments and Investment income. Operating costs (adjusted for non-cash items such as the USS deficit recovery provision and revaluation of the CPI-linked bond) have increased by 5%, primarily as a result of increased Estates and other operating expenditures, in both staff and other operating costs, in the Academic University, and increased Press & Assessment activity. The impact of continuing inflation has been seen across a broad spectrum of the Group’s cost base.

Total income is higher year on year with an increase of 4% compared to 2023, driven by increases in all categories except funding body grants. Higher income in the Press & Assessment and increased tuition fees and education contracts, donations and endowments, and investment income are the primary drivers, with smaller increases in other income, and research grants and contracts income.

|

|

2023–24 £m |

2022–23 £m |

Change % |

|

Income |

2,631 |

2,518 |

4% |

|

Expenditure excluding non-cash USS pension and CPI bond adjustments |

(2,601) |

(2,479) |

5% |

|

Non-cash USS pension and CPI-bond adjustments* |

357 |

161 |

|

|

Surplus before other gains and losses and share of surplus of joint ventures and associates |

387 |

200 |

94% |

|

Loss on disposal of fixed assets |

(1) |

– |

|

|

Gain on investments (net) |

346 |

4 |

|

|

Taxation |

(6) |

(5) |

|

|

Surplus for the year |

726 |

199 |

265% |

|

Actuarial gain |

99 |

286 |

|

|

Loss on foreign currency translation |

– |

(6) |

|

|

Total comprehensive income for the year |

824 |

479 |

74% |

|

|

2023–24 £m |

2022–23 £m |

|

|

Surplus for the year (as above) |

726 |

199 |

|

|

Less: Gain on investments |

(346) |

(4) |

|

|

Less: CPI-linked bond fair value adjustment |

(13) |

(85) |

|

|

Less: USS pension deficit recovery reflected in staff costs |

(344) |

(75) |

|

|

Less: Donation, endowment and capital grant income |

(190) |

(182) |

|

|

Add: CUEF income (distribution basis) |

152 |

138 |

|

|

Adjusted operating deficit for the year** |

(16) |

(10) |

|

|

2023–24 £m |

2022–23 £m |

|

|

Adjusted operating deficit for the year (as above) |

(16) |

(10) |

|

|

Less: the Press & Assessment adjusted operating surplus |

(175) |

(133) |

|

|

Less: Trusts and other adjusted operating deficit |

7 |

32 |

|

|

Less: CUEF operating deficit |

10 |

6 |

|

|

Add back: the Press & Assessment contribution to Academic University |

64 |

39 |

|

|

Other consolidation adjustments |

5 |

(7) |

|

|

Academic University adjusted operating deficit (Table 2) |

(105) |

(73) |

*Includes the non-cash credit relating to the USS deficit recovery provision of £344.3m (2023: £75.2m) related to the 2023 scheme valuation, and the positive impact of an unrealised non-cash credit of £13.2m (2023: £85.4m) related to the fair value adjustment to the CPI-linked bond.

**See Appendix 1 (p. 377) to the financial statements for further details.

Totals in the table above may not cast or cross-cast due to rounding.

The Group reported a surplus for the year of £726.1m (2023: £198.9m). The surplus is £527.2m higher than last year primarily reflecting the following:

•A significant non-cash credit of £344.3m (2023: £75.2m) relating to the USS scheme deficit recovery provision, based on the 2023 scheme valuation.

•Materially increased net gains on investments (other investments and investment property) of £346.4m (2023: £3.9m). Significant contributions included gains of £285.0m from the CUEF (2023: £83.8m), and from the Cambridge Multi-Asset Fund (CMAF) of £50.5m (2023: £12.1m). There were also smaller gains from Spin-out companies and other securities of £6.0m (2023: loss of £26.9m) and current asset investments of £7.3m (2023: loss of £2.6m). Investment property valuations were relatively stable with a revaluation loss of £2.4m, compared with a loss in 2023 of £62.5m which was primarily as a result of changes in key worker housing ratios and increasing build and infrastructure costs at the Eddington development.

•A fair value adjustment relating to the CPI-linked bond amounting to a credit of £13.2m (2023: £85.4m).

•An overall increase in the underlying cost base of the Group ahead of the increase in recurring revenues (excluding restricted endowments and donations, including those for multi-year programmes and capital donations).

Group total comprehensive income for the year is £823.6m (2023: £479.0m), which results from the surplus of £726.1m, and £98.6m of actuarial gains (2023: £286.4m), derived from the Group’s defined benefit pension schemes, primarily reflecting the impact of changing demographic assumptions during the year, and a higher return on scheme assets.

Unrealised gains/losses on investments, fair value adjustment of the CPI-linked bond, actuarial gains and losses on pension schemes and donations, endowments and capital grant income will continue to fluctuate from year to year over time. These effects are demonstrated in the historical trend data (see Appendix 1). The University considers a meaningful, reliable measure of underlying recurrent operating performance to be the adjusted operating surplus/(deficit) for the year, being the surplus for the year adjusted for gains and losses on investments, the CPI-linked bond fair value adjustment, the change in USS pension deficit recovery provision, donations, endowments, and capital grant income, and the CUEF income on a distribution basis. The Group had an increased adjusted operating deficit this year, largely as a result of the changes in income and expenditure described later in this review. The Academic University’s operating cash flows are supported by the element of CUEF distributions funded from long-term capital growth, subsidising the deficit on core teaching and research activities.

Investment by the Group in its capital infrastructure continued during the year, with £171.6m (2023: £177.4m) invested in fixed assets, software, and investment property over the period. The overall investment programme activity remains largely on track during the year.

On a Group basis, the underlying 2024 financial operating performance was satisfactory. The significant cost pressures evident in the prior year have continued this year and will require careful management in the higher cost environment in which the Group now operates. Management regard the most representative measure of underlying performance to be the adjusted operating deficit for the year of £15.7m (2023: £9.5m) reflected above and in Appendix 1 to the financial statements.

The consolidated position comprises four main segments: (i) core academic activities of the Academic University; (ii) the assessment and publishing activities carried out by the Press & Assessment; (iii) CUEF, the investment fund managed by the Group and holding the majority of the Group’s investments together with some investments of Colleges and other associated bodies; and (iv) the combination of smaller entities including the associated trusts and subsidiary companies not included in the other segments. Within the Group, there are a number of intra-group transactions, principally the financial and other support from the Press & Assessment and the CUEF distribution from capital growth. Table 2 gives segmental information, which is considered in further detail in Note 19 to the financial statements.

|

TABLE 2 |

2023–24 |

|||||

|

2024 £m |

The Press & Assessment 2024 £m |

CUEF 2024 £m |

Trusts and other 2024 £m |

Elimination and adjustments* 2024 £m |

Total 2024 £m |

|

|

Income** |

1,696 |

1,047 |

31 |

170 |

(313) |

2,631 |

|

Expenditure |

(1,306) |

(832) |

(41) |

(158) |

93 |

(2,244) |

|

Surplus / (deficit) before other gains and losses and share of surplus of joint ventures and associates |

390 |

215 |

(10) |

12 |

(220) |

387 |

|

Loss on disposal of fixed assets |

(1) |

– |

– |

– |

– |

(1) |

|

Losses / (gains) on investments (including CUEF gain) |

151 |

27 |

312 |

12 |

(156) |

346 |

|

Taxation |

– |

(6) |

– |

– |

– |

(6) |

|

Surplus for the year*** |

540 |

236 |

302 |

24 |

(376) |

726 |

|

Gain on investments |

(151) |

(27) |

(312) |

(12) |

156 |

(346) |

|

Less: CPI-linked bond fair value adjustment |

(13) |

– |

– |

– |

– |

(13) |

|

Less: USS pension deficit recovery provision |

(303) |

(34) |

– |

(7) |

– |

(344) |

|

Less: Donation, endowment, and capital grant income |

(178) |

– |

– |

(12) |

(1) |

(190) |

|

Add: CUEF income (distribution basis) |

– |

– |

152 |

– |

– |

152 |

|

Adjusted operating (deficit) / surplus for the year ** |

(105) |

175 |

142 |

(7) |

(221) |

(16) |

|

2022–23 |

||||||

|

2023 £m |

The Press & Assessment 2023 £m |

CUEF 2023 £m |

Trusts and other 2023 £m |

Elimination and adjustments* 2023 £m |

Total 2023 £m |

|

|

Income** |

1,589 |

1,015 |

21 |

172 |

(278) |

2,518 |

|

Expenditure |

(1,337) |

(873) |

(27) |

(189) |

108 |

(2,318) |

|

Surplus / (deficit) before other gains and losses and share of surplus of joint ventures and associates |

252 |

142 |

(6) |

(17) |

(171) |

200 |

|

Losses / (gains) on investments (including CUEF gain) |

(110) |

6 |

92 |

(32) |

48 |

4 |

|

Taxation |

– |

(5) |

– |

– |

– |

(5) |

|

Surplus for the year*** |

142 |

143 |

86 |

(49) |

(123) |

199 |

|

Less: Loss / (gain) on investments |

110 |

(6) |

(92) |

32 |

(48) |

(4) |

|

Less: CPI-linked bond fair value adjustment |

(85) |

– |

– |

– |

– |

(85) |

|

Less: USS pension deficit recovery provision |

(73) |

(3) |

– |

1 |

– |

(75) |

|

Less: Donation, endowment, and capital grant income |

(166) |

– |

– |

(16) |

– |

(182) |

|

Add: CUEF income (distribution basis) |

– |

– |

138 |

– |

– |

138 |

|

Adjusted operating (deficit) / surplus for the year ** |

(73) |

134 |

132 |

(32) |

(171) |

(10) |

*Includes elimination on consolidation of the Press & Assessment transfers, CUEF distribution from capital growth, and other consolidation adjustments.

**Income includes distribution from CUEF as income, which is eliminated at consolidated level.

*** Surplus for the year for the Press & Assessment is before distribution to the Academic University.

Totals in the tables above may not cast or cross-cast due to rounding.

The Group’s income increased by £112.4m (up 4%) from £2,518.3m to £2,630.7m. The Group has diversified sources of revenue providing operational stability with a compound growth of 5.7% over a rolling 10‑year period. The increase this year has come from the continued growth in examination, assessment and publishing services, with an increase of £25.8m (3%) during the year, reflecting continued growth in the business since the merger of the Press and Assessment businesses in 2021. Donations and endowment income, other income, and investment income have also increased significantly, with smaller increases in tuition fees and research grants and contracts income. Funding body grants have fallen by 2%.

•Revenues from examination, assessment and publishing services (comprising the majority of revenues from the Press & Assessment) represent the largest source of Group income, and in aggregate totalled £1,016.8m (2023: £991.0m), which amounts to 39% of total Group revenues for the year.

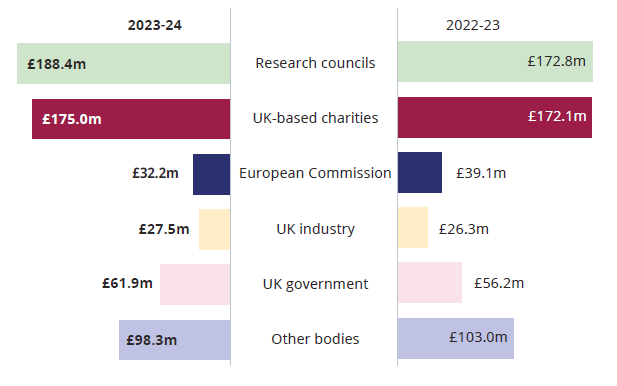

•Sponsors of research projects represent the second largest source of income for the Group. Research grants and contracts increased by 2% this year to £583.3m (2023: £569.5m). The increase has mainly come from higher funding from Research Councils, which increased by 9%, or £15.6m, to £188.4m, with smaller changes in other funder groups broadly offsetting each other.

•Tuition fees and education contracts totalled £415.3m (2023: £390.1m), up 6%, principally due to increases in non‑regulated fees.

•Funding body grants from the OfS and Research England decreased by 2% to £202.5m (2023: £207.6m), the majority of which related to recurrent research grants and grants for capital expenditure.

•Other income of £188.5m (2023: £178.0m) increased this year, with higher revenues from residences, catering, conferences, and a continued recovery in revenues from the Group’s various non‑core activities related to academic departments.

•Donations and endowments received were £150.2m (2023: £132.4m), with the increase primarily due to significantly increased new academic university endowments, which increased to £38.3m from £10.5m the previous year, and recognition of the Dell Corporation equipment donation for the Dawn AI supercomputer. This was offset by lower restricted donations for multi-year projects, and reduced donations of heritage assets during the year of £6.5m (2023: £19.1m).

•Investment income increased to £74.1m from £49.7m in 2023, primarily as a result of increased income from short‑term and fixed‑rate deposits, with the impact of increased interest rates having impacted in full this year, and only part of the previous year. Investment income from the CUEF also increased significantly.

The Press & Assessment carry out examination and assessment services through its three exam boards: Cambridge Assessment English, Cambridge Assessment International Education, and Oxford Cambridge and RSA Examinations (OCR). Publishing services incorporate income from the sales of educational and scholarly books, e-books, journals, applications, and related services through its three publishing groups: Academic (research books, advanced learning materials and reference content as well as journals); Cambridge English Language Teaching (materials for both adults and students); and Education (teaching materials for schools and advice on educational reform). Total examination, assessment and publishing income in the year to 31 July 2024 increased by 3% to £1,016.8m as noted above, representing continued solid growth post the merger of the Press and Assessment businesses in 2021.

The Group’s research income increased to £583.3m from £569.5m in the previous year. The increase has mainly come from higher funding from Research Councils, which increased by 9%, or £15.6m. In other categories, there were small percentage increases in UK Industry, UK‑based charities and UK Government offsetting a fall of 18% in funding from the European Commission.

The University receives recurrent funding from the UK government in the form of grants for teaching, research, and other activities. The University was also allocated £139.9m (2023: £141.5m) of Quality-Related (QR) funding, representing 7.1% (2023: 7.2%) of the overall grant award for England.

The University receives benefactions and donations from a variety of sources including trusts and foundations, corporations, and individuals (both alumni and non-alumni). The total given for donations and endowment income recognises all new endowments, donations for capital in respect of heritage assets, and other restricted and unrestricted donations available for current spend.

In aggregate over the year ended 31 July 2024, donations and endowment income totalled £150.2m (2023: £132.4m). Whilst the level of donations available for unrestricted purposes was slightly below the previous year, there was a significant increase in new academic university endowments, which increased to £38.3m from £10.5m the previous year. This was offset by lower restricted donations for multi-year projects, primarily due to lower donations for the Mastercard Foundation Scholars programme, and reduced donations of heritage assets during the year of £6.5m (2023: £19.1m). Dell Corporation also made an equipment donation for the Dawn AI supercomputer, the estimated fair value of which was recognised as income in the current year.

The Academic University continues to see increasing benefits from the dedicated team of development professionals, working in alignment with the University’s priorities in raising endowment and investing in cutting-edge research, scholarships, and facilities. In July 2022, the Dear World, Yours Cambridge Campaign for the University and Colleges concluded, raising a total of £2.217bn in commitments. With reference to international competitors’ philanthropy programmes, the University continues to develop the potential to grow donations, with enhanced alignment to academic priorities.

Investment income is an important component of the University’s funding mix generated by the Group’s financial investments, in particular the CUEF and from current asset investments (deposits and money market investments). During the year, the Group invested a further £150m in the Cambridge Multi-Asset Fund (CMAF), which is intended to provide greater returns than deposits and money market investments, whilst maintaining high levels of liquidity for funds intended for operational use, over the medium term. The Group has reported investment income of £74.1m (2023: £49.7m).

Other investment assets (excluding CUEF assets) generated income of £43.1m during the year (2023: £29.1m), mainly from cash and money-market deposits. The majority of the University and Group’s current asset investments are invested in the deposit pool. This pool is managed by the Group Treasury according to guidelines on diversification, exposure, and credit quality as agreed by the Finance Committee. The investments are principally short-term deposits with banks and similar institutions. The year on year increase in income is primarily due to the impact of the Bank of England base rate, which impacts institutional cash and money market deposit rates, being at 5.00–5.25% for the full year, compared to the prior year where rates climbed progressively from 1.25% at the start of the year to 5.00% by the end.

Investment income from the CUEF also increased from £20.6m to £31.0m.

The Group generates significant other income including property rentals, contributions from health and hospital authorities, residences, catering and conferences, other activities linked to academic departments (for example, the Cambridge Institute for Sustainability Leadership) and income from intellectual property managed, primarily, through Cambridge Enterprise Limited. Total other income of £188.5m (2023: £178.0m) has increased this year, primarily as a result of continued recovery in residences, catering and conferences, and other activities linked to academic departments.

The Group’s headline total expenditure of £2,243.7m (2023: £2,317.9m) was £74.2m lower than the prior year. However, excluding the non-cash impacts of significant adjustments to the USS deficit recovery provision and the fair value adjustment related to the CPI-linked bond described on p. 296, expenditure was £2,601.2m (2023: £2,478.5m), an increase of £122.7m (5%) compared to the prior year.

Expenditure excluding the USS deficit recovery provision adjustment, and the fair value adjustment related to the CPI‑linked bond, comprises staff costs (including research) of 45%; other operating expenses of 48%; depreciation and amortisation of 6%; and interest and other finance costs of 1%. The main changes compared to 2023 levels reflect the following:

•Staff costs increased by 7% to £1,171.0m (2023: £1,095.8m). The increase is substantially due to a mix of an increase in staff numbers, with full-time equivalent (FTE) staff increases of approximately 4–6% across the Group’s operating segments, and pay increases, both relating to the national higher education pay settlement and increases in pay for staff working in the Group’s commercial activities.

•Other operating expenses increased by 4% to £1,245.1m (2023: £1,197.7m), reflecting increased costs in the Academic University (primarily Estates and buildings, travel and transport, and IT services and equipment), and to a lesser extent the Press & Assessment (increases in both cost of sales and other operating costs, related to the increase in income described on p. 298).

•Depreciation and amortisation has increased from £136.4m to £151.6m.

•Excluding the CPI bond fair value adjustment, Interest and other finance costs of £33.5m (2023: £48.6m) mainly comprise Interest payments on bonds of £21.2m (2023: £21.1m) and other interest costs, primarily relating to non-cash interest on pension liabilities of £11.8m (2023: £26.3m), which has decreased due to the impact of favourable movements in bond yields on scheme discount rates.

During the year, the net cash outflow from operating activities after taxation of £58.3m was significantly adverse to the prior year (2023: inflow of £26.0m). Much of the outflow relates to working capital, where there was an outflow of £63.1m, compared to an outflow of £41.7m in 2023. Movements in both debtors (in both the Academic University and the Press & Assessment) and creditors (primarily research received in advance in the Academic University) contributed to the position.

A significant driver of the adverse variance resulted from the operating cost base (excluding non‑cash items) of the Academic University rising significantly faster than operating income, contributing to the increased adjusted operating deficit noted in Table 2 on page 297, partly offset by the increased surplus generated by the Press & Assessment. The activities of the Press & Assessment further the mission of the University in important ways and provide significant sources of funds for the Academic University. In the financial year to 31 July 2024, the Press & Assessment produced an increased surplus (before contribution to the University) of £235.8m (2023: £143.2m), although the current year included a material non-cash credit adjustment relating to the USS pension scheme deficit recovery provision of £34.4m. Routinely, 30% of these surpluses are transferred to the University and used towards funding capital expenditure and academic investment, alongside donations, grants, and a continued draw on University unrestricted resources.

The net cash inflow for the Group was £216.5m (2023: outflow of £209.6m), driven by net cash outflows from operating activities after taxation as noted above of £58.3m, cash inflows from investment activities of £219.3m (2023: outflow of £237.3m) and inflow from financing activities of £55.5m (2023: inflow of £1.7m). The inflow from investment activities relates primarily to an increase in CUEF cash balances from movements between investment assets and cash and of £213.2m, net disposals of other current assets (primarily money market funds with greater than three months duration at inception) of £146.6m, capital grants and donations income of £52.2m, offset by fixed and intangible asset purchases of £144.3m and a further investment of £150m into the Cambridge Multi Asset Fund (CMAF). The inflow from financing activities is primarily related to new endowment income of £38.3m and further secured borrowings of the CUEF of £36.9m, net of bond interest payments of £21.0m.

The following table shows the movement in Group net assets analysed into its main segments:

|

TABLE 3 |

Academic University 2024 £m |

The Press & Assessment 2024 £m |

CUEF 2024 £m |

Trusts and other 2024 £m |

Elimination and adjustments 2024 £m |

Total 2024 £m |

|

Net assets at 31 July 2023 |

5,663 |

961 |

4,087 |

556 |

(4,099) |

7,168 |

|

Surplus / (deficit) for the year before tax |

540 |

242 |

302 |

24 |

(376) |

732 |

|

Taxation |

– |

(6) |

– |

– |

– |

(6) |

|

Surplus for the year (Table 2) |

540 |

236 |

302 |

24 |

(376) |

726 |

|

Actuarial gain |

85 |

13 |

– |

– |

– |

99 |

|

Loss on currency translation |

– |

(1) |

– |

– |

– |

(1) |

|

Transfers |

– |

(64) |

(103) |

(10) |

177 |

– |

|

Net assets at 31 July 2024 |

6,288 |

1,145 |

4,286 |

570 |

(4,298) |

7,991 |

Totals in the table above may not cast or cross-cast due to rounding.

The Group’s net assets totalled £7,991.0m at 31 July 2024 (2023: £7,167.7m). Total comprehensive income of £823.6m (2023: £479.0m), comprising the majority of the increase in net assets, is described on p. 296.

The University has continued to deliver its capital investment programme, focusing on maintaining and enhancing its facilities and infrastructure in order to safeguard its position as a global leader in education and research. However, cash generated from the University’s own operational activities continues to be insufficient to deliver significant elements of the programme. For this reason, philanthropy and other sources of capital funding, including contributions from the Press & Assessment, are critical to the future programme’s success.

During the year, fixed asset additions for the Group were £111.1m (2023: £113.9m), with capital expenditure on Land and Buildings of £52.2m (2023: £73.5m), and further capitalisation of £58.9m (2023: £40.4m) on equipment. The University continues to complete the extensive capital investment programme of the last few years and focus on developing a sustainable mid- and long-term programme of investments in buildings, people, and infrastructure. The most significant land and buildings expenditure during the year related to completion of the new Cavendish III national laboratory facilities and the extension and upgrade to the Whittle Laboratory. These projects constituted 58% of the capital expenditure on Land and Buildings.

The University’s estates strategy is continuing to reshape the City. Focused on the major campus areas of West and North West Cambridge, the Biomedical Campus, and the City Centre, the estates strategy is supporting both continued academic excellence and the development of housing, transport, and childcare facilities for staff and their families. The University continues to develop its site at Eddington (formerly North West Cambridge), with Phase 1 now complete, and work continues on the options for future phases.

The Group has continued to invest in Intangible assets during the year, with capitalised expenditure of £50.5m (2023: £52.0m), the majority of which relates to software development in both the Press & Assessment, and Research, HR and Finance transformation programmes in the academic university.

The CUEF is an investment vehicle, which enables the University to pool assets held on trust and invest them for the very long term, gaining from scale, diversification and professional management. The CUEF is managed by University of Cambridge Investment Management Limited (‘UCIM’) under investment and distribution policies set by the Cambridge University Endowment Trustee Body (‘CUETB’) with input from its Investment Advisory Board. The CUEF is open to the University and to the Colleges and charitable trusts associated with the University. At 31 July 2024, there were sixteen College and five Trust investors.

The CUEF aims to preserve and grow the value of the perpetual capital of its investors, while providing a sustainable income stream. The investment strategy of the CUEF is primarily to invest through specialist, third‑party fund managers in order to access the various asset types and geographies that the Fund targets. A central tenet of the strategy is that well‑directed active management allows unconstrained investors with long‑term investment horizons to outperform passive investments over time, net of fees.

This contention has been supported by Fund performance over the life of the CUEF and aims to enable CUEF to meet its long-term return objective of the UK Consumer Prices Index (CPI) +5%, net of fees, to fund distributions to investors of around 4% of the net asset value per year. The distribution policy is based on underlying capital values, ensuring the distribution is directly linked to the performance of the Fund.

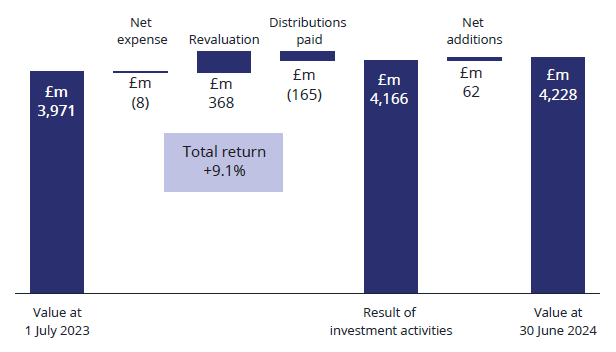

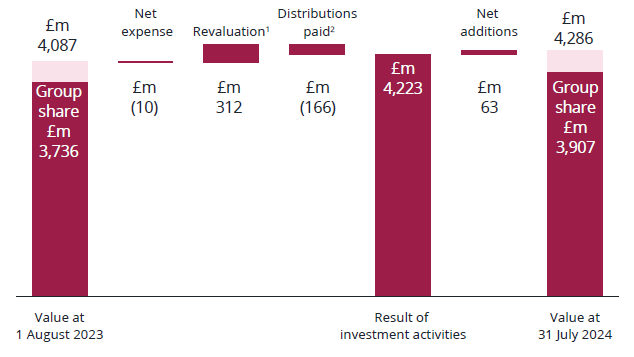

At 31 July 2024, the net asset value of the CUEF was £4,285.9m (2023: £4,087.2m) of which £3,906.7m (2023: £3,735.9m) is attributable to the Group.

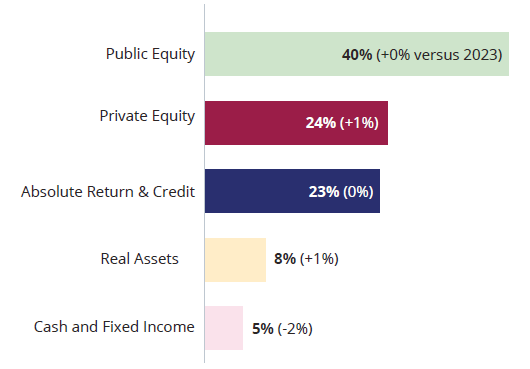

The Fund is diversified over five broad asset classes: Public Equity, Private Equity, Absolute Return & Credit, Real Assets, and Fixed Interest/Cash. Due to this diversification, the annualised volatility of the Fund has been approximately 60% of the MSCI All‑Country World Equity Index ex‑fossil fuels (‘ACWI ex-fossil fuels’) since 1 July 2020 as measured in Sterling. Direct investment by the Fund is modest and primarily focused on positions held to maintain an appropriate level of broad market exposure. These may include, from time to time, real estate, equity index positions, exchange traded funds, and instruments for the management of the Fund’s foreign exchange hedge programme.

The asset allocation and investment selection in the Fund is aimed at optimising the expected long-run total return, bearing in mind expected future volatility. The CUEF’s asset allocation as at 30 June 2024 is shown below. Over the course of 2024, allocations to Private Equity and Real Assets have increased in comparison to 2023; and allocation to Cash and Fixed Income has decreased.

The CUEF’s financial year ends on the 30 June. For this financial year ended 30 June 2024, the CUEF delivered a net return of +9.1% (2023: +4.1%), which is 2.0% above the Fund’s absolute target of CPI +5%. Since 1 July 2020, the date at which UCIM’s new investment approach was incepted, the CUEF has delivered an annualised return of +8.9%.

The University’s Financial Statements include the CUEF values and gains on investment on a 31 July basis. The overall CUEF movements are demonstrated below.

The University Group’s share of the CUEF represents approximately 91% of the total of £4,285.9m at 31 July 2024.

References:

1 Group share (Note 23) £285m.

2 Group share (Note 12) (£152m).

UCIM has continued to make encouraging progress towards its ambition of net zero greenhouse gas emissions from the CUEF portfolio by 2038, in line with the broader operational ambitions of the University.

The aim is to achieve this goal with a three-pronged strategy of:

•investing in renewable energy development and divesting meaningful* exposure to fossil fuels by 2030;

•engaging with the CUEF’s fund managers; holding them to account on reducing carbon emissions in their portfolios; and

•reporting regularly to stakeholders on progress against these aims.

* UCIM defines ‘meaningful’ as 0.5% of the portfolio or less.

Highlights in the year include:

•Development of new and enhanced frameworks to assess third-party asset managers’ sustainable investment activities, including a new framework to evaluate absolute return and credit managers and a substantial piece of research on voting and engagement best practice in public equities.

•Eight fund managers attended a bespoke executive education programme, in partnership with the Cambridge Institute for Sustainability Leadership (‘CISL’), focused on providing the frameworks and tools for them to reduce emissions from their portfolios. Following this cohort, 26 firms have completed the programme, representing approximately 40% of the net asset value of the CUEF. A fifth cohort is planned for 2025.

•As a result of UCIM’s engagement, a number of fund management partners have improved their sustainable investment policies and activities, more managers are measuring and reporting emissions from their portfolios, and one manager has accelerated its net zero ambition from 2050 to 2038, to align itself with the CUEF.

•UCIM further increased its level of engagement with University stakeholders, to improve awareness and understanding of UCIM’s sustainable investment strategy, including the Student Union, Green Officers, CUDAR, academic and other departments supported by the CUEF, as well as continuing to hold an annual, open ‘Town Hall’ event.

•The fourth year of the paid, six-week summer internship programme, for two University of Cambridge undergraduates to work on sustainable investment projects with UCIM’s investment team, was successfully completed.

Further information about the CUEF is available on the UCIM website: https://www.ucim.co.uk/.

Some long-term investments are held outside the CUEF, amounting to £185.1m (2023: £179.2m). These include other securities, JVs, associates, and equity investments in spin-out companies overseen by the University’s technology transfer company Cambridge Enterprise Limited and through its holding in Cambridge Innovation Capital. Investment gains of £6.2m primarily related to Cambridge Innovation Capital and other securities.

During the year, the Group invested a further £150.0m in the Cambridge Multi-Asset Fund (CMAF), which is intended to provide greater returns than deposits and money market investments, whilst maintaining high levels of liquidity for funds intended for operational use, over the medium term. The fund had a value of £607.4m at 31 July 2024 (2023: £406.8m).

The Group is exposed to the costs and risks of pension schemes, in particular in relation to the Universities Superannuation Scheme (USS). The USS is a multiemployer scheme and Note 36 to the financial statements describes how the scheme is reflected in these statements. Because of the mutual nature of the USS scheme, the University is unable to identify its share of the underlying assets and liabilities of the scheme on a consistent and reasonable basis. As required by FRS 102, the University, therefore, only recognises a balance sheet liability, where appropriate, in respect of future contributions arising from any agreed Recovery Plan, which determines how each employer within the scheme will fund a deficit where it arises.

The actuarial valuation of the overall scheme as at 31 March 2020 reflected a shortfall of £14.1bn, which was previously mitigated though an agreed Deficit Recovery Plan paid for by all institutions as per an agreed Schedule of Contributions. During the year, the 2023 actuarial valuation was finalised, and the resulting surplus of £7.4bn has led to the removal of the obligation to make deficit recovery contributions effective from 1 January 2024. As a result, the Group derecognised the brought forward provision of £348.9m in full during the year.

The Group has three other major schemes: the Cambridge University Assistants’ Contributory Pension Scheme (CPS) for University assistant staff and two defined benefit schemes for staff of the Press & Assessment.

These schemes, being single-employer schemes, are included in the financial statements in accordance with FRS 102 requirements for defined benefit scheme pensions accounting.

The CPS is a hybrid-defined benefit scheme, with a defined contribution component. The scheme remains open to new joiners and future accrual. The triennial valuation of the CPS at 31 July 2021 showed a significantly improved position, and the scheme is now in a surplus position of £17.8m (2023: deficit of £62.6m) for FRS 102 reporting purposes. The majority of the improvement is as a result of the impact of changing demographic assumptions during the year, and a higher return on scheme assets.

The University has recognised an asset in relation to the surplus position as the scheme is open to new members and accrual for existing members, and the University is able to recover the surplus through reduced future contributions. Since 2011, additional employer contributions of £14.6m p.a. have been made, but it was agreed that there would be no additional contribution during the year from 1 August 2023 to 31 July 2024.

The Press & Assessment defined benefit schemes are closed to new joiners and, following the triennial valuation of the two UK schemes as at 1 January 2022, show a substantially improved deficit position. Under FRS 102, the schemes are in a small, combined deficit position of £3.6m (2023: £16.8m).

Finally, there is a modest net pension asset recognised of £0.9m (2023: £0.8m) in respect of other pension schemes, including the Press & Assessment US schemes which have net assets of £2.7m (2023: £2.2m) and the Local Government Pension Scheme for staff who are employed through the University’s primary school. Pensions are discussed further in Note 36 to the financial statements.

The Group’s current service costs and deficit-recovery contributions (including the USS provision decrease) as reflected through staff costs were a credit of £195.3m (2023: charge of £78.4m). Excluding the non-cash adjustment to the USS provision, costs were £149.0m (2023: £181.4m), with the reduction primarily as a result of the fall in USS employer contributions effective from 1 January 2024 and reduced service costs for the CPS scheme.

In 2012, the University issued £350m of 3.75% unsecured bonds due in October 2052. The bonds are listed on the London Stock Exchange. The net proceeds of the issue (£342m) were applied in the University’s investment in the Eddington development.

In 2018, the University secured additional external finance, providing the University with options to further develop its non-operational estate (that is, projects outside those directly enabling core academic teaching and research activities). The University raised £600m in unsecured external finance through two tranches:

•£300m 60-year (2078) bullet repayment fixed-rate bond at coupon 2.35% p.a.

•£300m 50-year (2068) CPI-linked bond at coupon 0.25% p.a., amortising from year 10 and capped at 3% and floored at 0%.

As at 31 July 2024, the Group had outstanding bond liabilities totalling £824.5m (2023: £837.4m).

Over time, proceeds from the bonds will provide added flexibility in the continuing support of the University’s academic mission and furthering the interests of our students through the development of income-generating projects in the non-operational estate, including further strategic housing.

Such income-generating projects are of high strategic importance; they deliver significant indirect benefits essential to the University’s primary mission, while also addressing the critically important housing challenge, providing alternative income streams at a time of significant financial volatility.

The Group’s net debt as at 31 July 2024 was £84.2m (2023: £1.0m) (see Note 42). This includes the cumulative non‑cash fair value re‑measurement of the CPI‑linked bond at the balance sheet date of credit £113.5m (2023: £100.3m). This will move year on year depending on volatility in the bond markets, so a more reflective position of the Group’s underlying net debt position is an adjusted net debt of £242.6m (2023: £136.1m), taking into account the cumulative fair value remeasurement described above, and the accretion in the value of the CPI‑linked bond of £44.9m from inception. The change during the year is materially impacted by the investment of Group funds into the CMAF (£150.0m) during the year. Please refer to Appendix 1 for more information.

The University remains confident of its long-term financial sustainability. At a time of significant financial pressure in the UK Higher Education Sector, the University’s reputation, diverse income streams and strong and liquid balance sheet means that it is well positioned to manage the pressure. Nonetheless, within the academic university, the high levels of recent inflation and lack of equivalent growth in tuition fees and funding body grants mean that costs have risen faster than revenues, thereby reducing funds available for investment. The University is continuing in its efforts to achieve efficiencies in the short and medium term to free up funds for investment to allow it to remain a world leading institution.

Tuition fee income is expected to grow modestly, reflecting a gradual increase in the number of postgraduate students paying international fees and a rise in unregulated fee levels. The rise in the regulated home fee level from £9,250 to £9,535 will make a small contribution to overall growth, but this amount would still represent less than half of the underlying cost of providing Cambridge’s unique student experience.

Research grants and contracts income recognised is expected to continue its recovery to pre-pandemic levels as current multi-year grant awards are completed. However, the University continues to compete in a highly competitive market, and the long-term trajectory continues to depend on levels of Government funding for research, supported by the University’s very strong performance in the last Research Excellence Framework and continued strong rankings. Block grants for funding from UKRI are not expected to increase to match inflation.

Cambridge University Press & Assessment has seen a further strong business performance during the year with total revenues of over £1bn. The outlook for this business remains highly dependent on the global economy, the levels of international interest in learning and certification in English, and the use of international curricula in schools around the world. Prospects also hinge on the continued development of digital delivery capabilities in an increasingly competitive market.

Costs across the University Group rose sharply in 2023 and whilst inflation has moderated somewhat, the cost base has continued to increase in 2024, in a continuing elevated inflationary environment. External factors of higher national pay settlements and elevated prices of goods and services are adding to a continued growth in Cambridge’s own activity levels, as well as targeted increases in spend on maintenance and renewals across our large physical and IT estates. The increase in employer’s National Insurance announced in the UK budget will also add materially to the Group’s costs. A small proportion of these additional costs will be offset by the increase in the cap on domestic undergraduate fees. To these costs, we must add the investment needed to meet the University’s zero carbon objectives, the costs of which remain to be fully determined. These increasing costs are likely to be offset somewhat by the expected reductions in ongoing energy costs. The University continues to work on pathways towards its commitment to reduce energy-related emissions from its operational estate to absolute zero by 2048.

In order to address the residual cost escalation and to provide additional resources to invest in pay and other priorities, a number of ambitious modernisation and transformation programmes are now underway, which bring significant potential to increase the levels of efficiency and effectiveness of the devolved organisation, notably through a reimagined approach to collective professional services, greater leverage in procurement and purchasing of goods and services, and through improved usage of the physical estate.

The long-term growth objective of the CUEF remains at 5.0% +CPI. However, turbulence in financial markets in response to global events continues to highlight the potential for volatility in short to medium term investment returns.

Risks to future financial performance continue to include economic and mobility concerns resulting from geo-political events; Government actions to address the national deficit and debt; sustained cost inflation; further turbulence in financial markets impacting future CUEF and other investment returns.

The University Council, which is the University’s principal executive body, takes primary responsibility for ensuring the University has an effective and balanced enterprise risk management framework in place. Business risk management is at the core of the University’s overall system of internal controls and is designed to focus on and mitigate, to every extent possible, the most significant risk events that might adversely or beneficially affect the University’s ability to achieve its policies, aims and objectives.

The University is committed to ensuring that it has a robust and comprehensive system of risk management in line with the requirements of the Office for Students, and follows good practice in considering risk appetite in the context of the University’s academic mission, seeking to ensure an appropriate balance between risk aversion and opportunity capture. The business risk management approach identifies and appraises risks and opportunities in a systematic manner. Accountability and responsibility for risk mitigation is assigned to management across the devolved organisation. Managers are encouraged to implement good risk management practice across the University. The University makes conservative and prudent disclosure of the financial and non-financial implications of risks.

The Group has a risk management framework overseen by the Audit Committee, for which the Council has the ultimate responsibility. The Academic University and the Press & Assessment have separate risk management policies which are relevant to those entities. The framework is designed to allow the senior leadership team to consider the University’s key risks in a meaningful way and within the context of the University’s evolving priorities, prior to scrutiny and approval of the University Risk Register through the Audit Committee and Council.

The senior leadership team is responsible for identifying and managing risks across the University’s activities. The Council receives reports on the University’s risks at least biannually, and seeks assurances over risk management and controls from individuals identified as accountable for risks. The Council has delegated to the Audit Committee the responsibility for reviewing the University’s risk management processes to ensure that they are adequate and effective. The Audit Committee considers risk management as a standing item in its meetings to ensure routine monitoring, and will report to the Council on internal controls and alert the Council to any emerging issues as necessary. The Audit Committee also receives an annual opinion from the internal auditors on the adequacy and effectiveness of the University’s arrangements for risk management, control and governance , and provides assurance to Council on the adequacy and effectiveness of the University’s arrangements for risk management.

This year the internal auditors opinion provided reasonable assurance that the University’s arrangements for risk management and governance were adequate and effective. The internal auditors provided limited assurance that the University has an efficient and effective system of internal control on the basis that a larger number of focus areas had been identified through their work where the University is taking steps to further enhance controls. The Audit Committee confirms its assurance to the Council on the adequacy and effectiveness of the University’s arrangements for risk management, control, governance and value for money.

In parallel to the risk management framework, the University’s senior leadership team have identified a set of University risks. The University Risk Register identifies those risks that are considered to have a fundamental impact on the University’s ability to deliver its mission or to operate effectively.

The principal risks and uncertainties of the University are broadly consistent year on year. These risks have potential downstream impacts on a number of the other risk areas identified. The activities of the Press & Assessment are subject to the pressures of international competition. The Press & Assessment balance the need to reinvest sufficient of their operating surplus to thrive with the need to support the University’s core academic activities wherever possible.

The University remains comparatively well positioned in the sector to deal with financial risks. While costs across the University Group have risen sharply in the prolonged high-inflationary environment, revenue streams are well diversified, both in terms of revenue line and geographically. These sources of revenue provide significant resilience, as does the strong and liquid balance sheet, enabling the University to manage the unexpected over the short term, and time to make the necessary operating adjustments. The University is undertaking efficiency measures as described on p. 304. Furthermore, there are potential additional sources of revenue open to the University, albeit that the University chooses not to maximise surpluses.

|

Risk area |

Responses and actions |

|

Reputational and financial impact through failure to meet OfS and other stakeholder expectations for widening student access and ensuring effective participation; student dissatisfaction in the quality of their educational experience; failure to compete with international competitors especially in providing financial support for doctoral students, particularly through failure to obtain funding for Doctoral Training Programmes (DTPs); inadequate support for student mental health and wellbeing; failure to recruit the very best undergraduate and postgraduate students; failure to ensure that educational facilities are of an acceptable standard for a worldclass educational institution. |

•Implementation of the actions committed to in the University’s Access and Participation Plan agreed with the OfS (2020–21 to 2024–25). •Full engagement with Colleges which are responsible for undergraduate admission decisions. •Implementation of the recommendations of the strategic review of admissions and outreach. •Continued progress in the Student Support Initiative with a particular focus on postgraduate studentships. •International Student Recruitment Strategy. •Support for innovation in methods of teaching and examination. •Implementation of the strategic review of student mental health and wellbeing. •Programme Board for Education Space responsible for improving educational space. •Strategy to support DTPs and Centres for Doctoral Training (CDTs). |

|

Significant downturn in UK and/or Global

financial markets leads to reduced financial

strength. Combined impact of

devalued long-term Investments, reduced endowment distribution levels,

deterioration in pension valuations (increasing contribution levels), levels

of student applications, particularly from overseas, and reduced sources of

revenue and philanthropy. Also further potential impact on staff through UK cost of living crisis and falling real incomes and potential supply chain disruption. |

•The University continues to focus on the optimal management of long-term financial sustainability, including stress testing and enhanced contingency planning. •The University is actively exploring opportunities to attract new revenue streams, modernise processes to seek cost efficiencies and ensure its capital programme is fully funded ahead of new commitments being made. •In the near term, the University is undertaking measures to drive operating efficiencies, in order to address the operational deficit in the Academic University ahead of more significant efficiencies expected to be realised through the ongoing transformation programmes. •Over time, more fundamental adjustments to the cost base could be made but would negatively impact on students and research. Likewise capital investment would have to be prioritised on refurbishment over investment. •The University is investing further in its Development and Alumni Relations activities. •The professionally managed CUEF has allocations across a diversified range of asset classes, sectors, styles and geographies with a broad equity focus, designed to optimise returns and be resilient over the long term. |

|

Significant increases in or continued high levels of inflation would result in an increase in the cost base of the University without matching increases in home student and government revenue streams. |

•The University will continue to engage with Government directly and through the HE sector to ensure the funding is allocated reflecting inflationary pressures and increased costs of services for the sector. •The University will continue to explore other revenue streams (both in the UK and internationally) with Cambridge University Press & Assessment to ensure the resources are maximised to offset increased costs. •The University will continue to invest in measures to increase the effectiveness and efficiency of its operations to optimise current and future use of resources. •The University will continue to monitor the USS pension scheme funding position, noting the improved position in recent monitoring reports. |

|

Changes to government policy particularly resulting from increased funding pressures related to UK national deficits and debt lead to further cuts in financial support and provision for education. |

•The University continues to engage with government directly and through the HE sector to influence policy in support of its education and research mission. The University also continues to diversify its income sources. •The University will continue to ensure REF preparedness across the University to maximise future QR funding opportunities. •The College dimension of education provision is distinctive and successful, but it is costly to deliver. The University continues to review ways of controlling costs, seeking value-for-money gains, and opportunities to develop the mix of students over time, while maintaining the highest quality of education and without compromising on admission standards. •The University will continue to maintain and further develop its strategic relationships with research funders, including charities, Research Councils and industrial funders, and respond to new funding opportunities as they arise. |

|

The Press & Assessment operates in

challenging international markets where global economic conditions and

competitor activity may adversely impact its financial

performance, reducing the funds available for reinvestment in

the University’s core academic

mission. The University has a wide international footprint of activities. International tax laws are narrowing the distinction between supporting activities and permanent establishments, leading to the potential for more overseas activity to become taxable. |

•The Press & Assessment is focused on the growing desire from learners, teachers and researchers to engage with Cambridge in a joined up digital way, and reflects the demand for innovative products that combine expertise in learning and assessment. Successfully competing in digital education is key to the Press & Assessment’s future success. •The Press & Assessment aims to diversify its product offerings, develop new revenue streams and deepen existing capabilities overseen by a Board with significant commercial expertise. •The University continues to monitor the key risks associated with its combined international activities. •The Strategic Partnership Office coordinates functional due diligence of proposed new international activities. •The University leverages specialist external taxation and legal advice in support of its core internal capabilities. |

|

Increasingly competitive landscape for all forms of research funding. |

•The University continues to enhance the capabilities and capacity of its Research Office in support of the ongoing processes for grant application and lifecycle management, compliance and enhancement of financial analysis. •The University continues to maintain active communications with key stakeholders (e.g. Research England, UKRI) and to diversify research income, including building on progress with philanthropy. •The University has a growing focus on industrial research collaboration with international partners, focusing on finding solutions to the major global challenges. |

|

Post-Brexit outcomes restrict

access to movement and funding of EU students and staff. Reduced access to

current levels of EU Research income. Wider economic downturn impacts future

sources of revenue and availability of indirect labour and materials,

disrupting the capital expenditure

programme. Areas of high-risk are: EU research funding, immigration costs, EU student recruitment, student funding and communications. |

•The ongoing financial and labour market challenges due to the UK’s exit from the EU remain of concern. The University and the HE sector continue to engage with Government on all post-Brexit issues. •Decrease in European Research Council (ERC) funding could still impact the University’s research income and its ability to engage leading researchers. •Managing the expectation of research projects due to increased costs of goods and services from EU as well as shortages of skilled labour to deliver these projects. |

|

Inability to attract and retain the best academics and adequately resource professional staff through a failure to compete with escalating levels of international reward levels, growth in the University’s complexity and scale, and high costs of living and housing in the Cambridge area. |

•The University continues to focus on pensions and pay as key components of a competitive employment proposition, seeking economy, efficiency and effectiveness in its operations to accommodate pay and pension inflation as necessary. •The University implemented part of the 2023–24 sector-agreed pay award in February 2023, six months early. The University will continue to monitor, and where appropriate address, the UK cost of living crisis impacting its staff. Further targeted pay measures are under consideration in parallel with the sector-wide national agreements. A package for 2024–25 has been agreed as the first step in a multi-year plan to improve pay and grading structures. Initial steps include a 2.5% supplement for staff on lower pay spine points. •The University is also focusing on the provision of transport, nursery schooling and housing, with the Eddington development designed to ease pressures. •The University continues to work with the sector to ensure long-term and attractive pension schemes including the USS. •The University is offering a flexible working environment. |

|

Significant data breach, failure to comply with GDPR, or major information security event (cyber security) leads to loss of confidential/commercially sensitive information or failure of IT infrastructure. |

•The University has invested resources to understand its data assets and the security landscape across a devolved institution, and to enable assessment of the risks associated with loss of confidential and commercially sensitive information. •The University has developed and is implementing an updated Cyber Strategy to deliver enhanced security controls across the University, noting that this is a challenge in more devolved areas of control and in an environment of increased and changing threats. •Further to specific cyber incidents during the year, the opportunity has been taken to accelerate the mandated option of key security measures. •The University has an ongoing programme of cyber risk awareness training and engagement for all staff. |

|

Inadequate long-term maintenance and

development of the academic and non‑academic estate and

supporting infrastructure. Failure to develop and protect a fit‑for‑purpose IT infrastructure due to devolved organisation and associated fragmentation, customisation and local solution development. |

•The University has an ambitious capital building programme and is actively sharpening the prioritisation and management of its strategic investments. •The University seeks to optimise available funding through maximising associated capital grants and philanthropic resources and by increasing net operating cash flows. •A comprehensive programme of work is continuing, aimed at tackling the maintenance backlog. Allocated funds for maintenance have been substantially enhanced to enable this work to build momentum. •From a strategic perspective, the Reshaping our Estate programme aims to create a University of Cambridge estate that is more efficient, more effective, more environmentally sustainable and fit for purpose. •The University continues to implement a Digital Workplace programme, with regular reports to the Audit Committee. This will include the adoption of a determined direction of travel to include: consistent and secure infrastructure agnostic of location; appropriate policies and standards for staff to work securely and effectively from any location; and a path to maximise the benefits offered by digital technologies. •Establish appropriate investment levels and the prioritised allocation of resources between the University’s digital vs. physical estate. |

|

Failure to maintain adequate risk management of Health & Safety related risks and compliance with associated regulations across the distributed University estate and activities leads to personal injury/fatality or significant loss of facilities. |

•The University has policies and procedures in place to support appropriate risk management and compliance across the organisation for Health and Safety related risks. However, the devolved nature of the University and diverse nature of associated direct and indirect activities represent a challenge in ensuring full assurance coverage. The University has strengthened its central oversight and governance of health and safety risks, one aim of which is to provide greater visibility of, and therefore assurance around, health and safety matters across the institution. |

The UK Higher Education sector is facing some significant financial challenges for two principal reasons. Firstly, cost inflation has far outstripped increases in tuition fees and funding body grants for research and teaching. Secondly, many institutions had expanded rapidly based on an assumption of ever-growing international student numbers, and rather than increase in 2024–25, it is likely that many institutions will see a decline. The University is exposed to the first effect but not, to any material extent, the second.

At Cambridge, we benefit from a diversified mix of revenues, and while we have not grown international student numbers and revenues in the past as fast as many other UK institutions, this leaves us less exposed to a downturn. We are fortunate to benefit from continued growth in Cambridge University Press & Assessment, a highly performing endowment and high levels of philanthropy for a UK University. We have also maintained a strong and liquid balance sheet. The University therefore remains in a strong financial position.

Nonetheless, we cannot be complacent. Cambridge has suffered from cost increases exceeding revenue growth within the Academic University increasing its operating deficit and this has necessitated a diversion of resources to meet this deficit that would otherwise have been available for investment. The mission of the University of Cambridge is to contribute to society through the pursuit of education, learning and research at the highest international levels of excellence. Continuing to operate at the highest international levels of excellence requires us to continue to invest in our people and our digital and physical estate, including decarbonisation.

We are therefore embarking on a multi-year programme to modernise our systems and processes to achieve efficiencies and provide more accurate and timely information allowing better decision making within our highly devolved organisation.

We are also close to completing a long-term integrated investment plan that will ensure that as we generate funds for investment, they are used to maximum effect in pursuit of our academic mission.

The University of Cambridge is in a solid financial position and if we can work together to modernise our systems and processes and achieve efficiencies, we can look forward with confidence to leaving the University in a strong position to remain a leading global institution.

Anthony Odgers

Chief Financial

Officer

1. The following statement is provided by the Council to enable readers of the financial statements to obtain a better understanding of the arrangements in the University for the management of its resources and for audit.

This statement relates to the period covered by the financial statements, and the period up to the date of approval of the audited financial statements.

2. The University endeavours to conduct its business in accordance with the seven principles identified by the Committee on Standards in Public Life (selflessness, integrity, objectivity, accountability, openness, honesty and leadership). The University complies with the voluntary Higher Education Code of Governance as revised in September 2020 by the Committee of University Chairs.

Under the University’s Statutes, the governing body of the University is the Regent House, which comprises some resident senior members of the University and the Colleges, together with the Chancellor, the High Steward, the Deputy High Steward, the Commissary and the external members of the Council. The approval of the Regent House is required for changes to the University’s Statutes and Ordinances and for any other matter for which, in Statute or Ordinance, the University’s approval must be obtained; the Council and the General Board may also decide to seek the Regent House’s approval on questions of policy, which are considered likely to be controversial. The Council of the University is the principal executive and policy-making body of the University, with general responsibility for the administration of the University, for the planning of its work, and for the management of its resources. The Council has a majority of internal members and is chaired by the Vice-Chancellor. Its membership includes four external members, one of whom chairs the Audit Committee (see paragraphs 4 and 7 below). The Statutes provide for the appointment of a Deputy Chair of the Council, normally one of the external members, to take the chair as necessary or when it would be inappropriate for the Vice-Chancellor to do so, in particular in relation to the Vice-Chancellor’s own accountability.

The General Board of the Faculties is responsible for the academic and educational policy of the University. The annual reports of the Council and the General Board are published on the University’s website and are submitted to the Regent House for comment and approval.

3. The University is an exempt charity and is subject to regulation by the Office for Students (OfS). The members of the University Council are the charity trustees and are responsible for ensuring compliance with charity law.

4. The Council is advised in carrying out its duties by a number of committees, including the Finance Committee, the Audit Committee, the Planning and Resources Committee, the Human Resources Committee, the Remuneration Committee, and the Committee on Benefactions and External and Legal Affairs. The Finance Committee advises the Council on the management of the University’s assets, including real property, monies and securities. The Audit Committee, which has a majority of external members, governs the work of the internal and external auditors, reporting on these matters directly to the Council. In addition, the Audit Committee reviews the University’s risk management processes to ensure that they are adequate and effective.

The Planning and Resources Committee (PRC) and the Human Resources Committee (HRC) are joint Committees of the Council and the General Board. The PRC’s responsibilities include the preparation of the University’s budget. The HRC advises the Council on matters concerning equality and diversity and equal and gender pay, providing an annual equality monitoring report, and on the policy framework governing staff-related matters, including the University’s policy on public disclosure (whistleblowing). The Remuneration Committee is chaired by an external member of the Council and approves market pay cases, incentive schemes and severance pay cases for senior staff as well as payments to external members of University bodies and committees. It provides advice to the Council on remuneration (including on compliance with the Higher Education Senior Staff Remuneration Code), succession planning and diversity, as appropriate, and it also reviews the University’s public disclosures relating to remuneration. The Committee on Benefactions and External and Legal Affairs (CBELA) considers matters likely to have an impact on the reputation of the University, including advising the Vice-Chancellor on the acceptability of donations. The Property Board oversees the development, management and stewardship of the University’s non-operational estate, including the commercial developments at Cambridge West and Eddington funded by bond issues. It reports to the Council’s Finance Committee. The Press and Assessment Board advises the Council on matters concerning the University Press & Assessment.

5. Under the terms of the OfS’ Terms and Conditions of funding for higher education institutions and the Terms and Conditions of the Research England grant between the University and the OfS, the Vice-Chancellor is the Accountable Officer of the University.

6. Under the University’s Statutes, it is the duty of the Council to exercise general supervision over the finances of all institutions in the University; to keep under review the University’s financial position and to make such reports thereon to the University as determined from time to time by Special Ordinance; to recommend bankers for appointment by the Regent House; and to prepare and publish the annual accounts of the University in accordance with UK‑applicable accounting standards such that the accounts give a true and fair view of the state of affairs of the University.

7. It is the duty of the Audit Committee to keep under review the University’s risk management strategy and implementation; to keep under review the effectiveness of the University’s internal systems of financial and other controls and governance; to advise the Council on the appointment of external and internal auditors; to consider reports submitted by the auditors, both external and internal; to monitor the implementation of recommendations made by the internal auditors; to satisfy itself that satisfactory arrangements are adopted throughout the University for promoting Value for Money (economy, efficiency and effectiveness); to monitor the University’s management and quality assurance of data submitted to the OfS and other bodies; to establish appropriate performance measures and to monitor the effectiveness of external and internal audit; to monitor incidences of fraud and other irregularities and their reporting to OfS as appropriate; to make an annual report to the Council and to receive reports from the OfS and other regulators. Membership of the Audit Committee includes, as a majority, five external members (including the Chair of the Committee), appointed by the Council with regard to their professional expertise and experience.

8. There are Registers of Interests of Members of the Council, the General Board, the Finance Committee, and the Audit Committee, and of the senior administrative officers. Declarations of interest are made via an annual declaration of interests process. In addition, interests that relate to particular agenda items are noted at the start of each meeting. All members of the Council were routinely asked to self‑certify against the OfS indicators of a ‘fit and proper person’ at the beginning of their tenure as trustees. Council members and senior officers are encouraged to have particular regard to the seven principles of public life, supported by the University’s management and governance arrangements.

The Chancellor:

Lord Sainsbury of Turville

The Vice-Chancellor:

Professor Deborah Prentice

Heads of the Colleges:

Professor Dame Madeleine Atkins

Mrs Heather Hancock

Professor Pippa

Rogerson (until 15 July 2024)

Sally Morgan, Baroness Morgan of Huyton

Professor Alan

Short (from 16 July 2024)

Professors, Clinical Professors, Readers and Professors (Grade 11):

Professor Jason Scott-Warren

Professor Anthony Davenport

Professor

Richard Mortier

Professor Sharon Peacock

Other members of the Regent House:

Dr Zoe Adams

Dr Ann Kaminski (until 31 October 2023)

Dr Mike Sewell

Dr Pieter van Houten

Ms Milly Bodfish

Mr John Dix

Dr Louise Joy

Mr Scott

Mandelbrote

Dr Ella McPherson (from 5 March 2024)

Student members:

Mr Sam Carling (until 30 June 2024)

Mr Fergus Kirman (until 30 June

2024)

Mr Vareesh Pratap (until 30 June 2024)

Ms Sarah Anderson (from 1 July 2024)

Mr

Sumouli Bhattacharjee (from 1 July 2024)

Mr Alex Myall (from 1 July 2024)

External members:

Ms Gaenor Bagley

Ms Sharon Flood

Professor Sir Alexander Halliday

Professor Andrew Wathey