No 6787

Wednesday 4 June 2025

Vol clv No 36

pp. 604–625

The Council and the General Board beg leave to report to the University as follows:

1. This Report proposes changes to Chapter III of Ordinances on the examination of taught programmes, to take effect from 1 October 2026. It marks the conclusion of the second and final phase of a review of examination regulations in light of the lessons learned during the 2023 marking and assessment boycott.

2. The review was conducted by a task and finish group chaired by Dr Pieter van Houten. Phase 1 of the review took forward the recommendations of the task and finish group in two areas:

(a)to articulate clearly the existing powers of the General Board to mitigate the impact of disruption to the examination process; and

(b)to revise Ordinances to include new measures to extend the General Board’s authority.

The Phase 1 recommendations were approved on 31 January 2025 following a ballot and were implemented with immediate effect.1

3. As Phase 2 of the review was expected to build on Phase 1, Phase 2 was paused to allow the ballot on Phase 1 to run its course. Work on Phase 2 resumed in February 2025, but with a necessary delay in the timeline for its implementation. The Phase 2 recommendations therefore take account of the changes made during Phase 1.

4. During Phase 2, the task and finish group broke down the terms of reference into the following points for review, resulting in the recommendations outlined below.2

(a) To consider whether some or all of the regulations should remain as Ordinances, subject to Regent House approval, or would more appropriately be located as regulations under the control of the General Board.

This Report does not propose that any parts of Chapter III should become General Board Regulations. However, there are some recommended changes to the Ordinances, as described below.

(b) To consider if other wider reforms as part of the re‑writing of Chapter III would be advantageous including devolving responsibility for the appointment of Examiners to Faculty Boards.

The changes to Ordinances propose that Examiner and Assessor appointments are devolved to Faculty Boards or comparable authorities with effect from 1 October 2026. This proposal reduces unnecessary administrative practice and sites responsibility for appointments with the most appropriate academic authority. If these changes are approved, the appointment process will be supported by the introduction of an automated examiner payment system. Training and guidance will be provided for both. This change is not expected to create more work than the current nomination process. No changes are proposed to the appointment of Chairs of Examiners, Senior Examiners and External Examiners, which will remain with the General Board on the recommendation of Faculty Boards or comparable authorities.

(c) To consider simplification and clarification of Ordinances in Chapter III, including whether some operational details should be removed and published in a different way.

Parts of Chapter III have been simplified and clarified by the removal of operational details. These details can more usefully sit outside of Ordinance to provide a degree of flexibility. These include:

(i)the dates by which entries of examination candidates and corrections of those entries are to be submitted;

(ii)the dates on which examinations shall be held;

(iii)the process for disclosure of examination marks;

(iv)the dates by which Faculty Boards and comparable authorities must make nominations for the appointment of Chairs of Examiners, Senior Examiners and External Examiners;

(v)the Schedules of payments to Examiners, Assessors and Supervisors who are and are not medically qualified.

The Examinations Office will provide the information online from 1 October 2026.

(d) To review regulations in the light of experience gained during the course of the marking and assessment boycott to ensure that regulations are clear. In particular, to achieve clarity around the appointment of Examiners, the approval and signing of class-lists, requirements for attendance at meetings, and arrangements in the case of Examiners being unable to attend.

Changes to Ordinances approved as part of Phase 1 have clarified the process for the signing of class-lists, the requirements for attendance at meetings, and the arrangements when Examiners are unable to attend meetings. See paragraph (b) above for recommendations concerning the appointment of Examiners.

(e) To consider what additional advice and guidance should be issued to Faculty Boards and Degree Committees, and to Chairs/Senior Examiners on their roles and responsibilities.

If this Report’s recommendations are approved, the available guidance will be reviewed in light of the changes. Existing advice and guidance, updated annually, is available on the Exam Operations SharePoint site,3 and covers:

(i)eligibility for all examining roles;

(ii)timelines for the appointment and nomination of all examining roles;

(iii)responsibilities and duties of each examining role;

(iv)requirements for Examiner meetings;

(v)Examiner absence;

(vi)payment criteria;

(vii)payment rates.

5. The Council and the General Board recommend that, with effect from 1 October 2026, the changes in Ordinance set out in Annex A be approved.

Deborah Prentice, Vice-Chancellor

Sarah Anderson

William Astle

Gaenor Bagley

Milly Bodfish

Daniela De Angelis

John Dix

Sharon Flood

Alex Halliday

Heather Hancock

Simon McDonald

Ella McPherson

Scott Mandelbrote

Ewa Marek

Sally Morgan

Alex Myall

Mezna Qato

Jason Scott-Warren

Alan Short

Pieter van Houten

Andrew Wathey

Garth Wells

Deborah Prentice, Vice‑Chancellor

Tim Harper

Ella McPherson

Patrick Maxwell

Nigel Peake

Richard Penty

Alan Short

Emily So

Pieter van Houten

Bhaskar Vira

Jocelyn Wyburd

1Reporter, 6750, 2023–24, p. 806; 2024–25: 6758, p. 102; 6769, p. 254.

2For the terms of reference of the review and the membership of the task and finish group, see Annex C of the Joint Report on Phase 1 (Reporter, 6750, 2023–24, p. 810). A tracked version of Chapter III of Ordinances is available at: https://www.admin.cam.ac.uk/reporter/2024-25/weekly/6787/Exams-ChapterIII-tracked.pdf.

3https://universityofcambridgecloud.sharepoint.com/sites/AD_ExamOperationsandMitigatingCircumstances (University Account required).

(a) By inserting the following new Ordinance, to appear at the beginning of Chapter III of Ordinances (Statutes and Ordinances, p. 254) to read as follows:

1. The Ordinances in this Chapter shall apply to the examination and assessment of all taught courses taken by matriculated students. The General Board shall maintain a list of those courses in the Schedule to this Ordinance, publishing such alterations as it sees fit.

2. The General Board shall publish and keep under review policies and procedures on the appointment, duties and payment of Examiners and others appointed under the Ordinance for the Appointment of Examiners and Other Appointments in the Examination Process, on the conduct of Examiner meetings, and on the disclosure of examination marks.[1]

Postgraduate Certificate in Education

Certificate of Postgraduate Study

All Diplomas

Bachelor of Arts

Bachelor of Medicine

Bachelor of Music

Bachelor of Surgery

Bachelor of Theology for Ministry

Bachelor of Veterinary Medicine

Bachelor of Divinity

Master of Accounting

Master of Advanced Study

Master of Architecture

Master of Business Administration (including the Executive M.B.A.)

Master of the Conservation of Easel Paintings

Master of Corporate Law

Master of Design

Master of Education

Master of Engineering

Master of Finance

Master of Law

Master of Letters

Master of Mathematics

Master of Music

Master of Natural Sciences

Master of Philosophy by advanced study

Master of Research

Master of Science

Master of Studies

Master of Surgery

[1] The policies and procedures are available on the Examinations Office website at: https://universityofcambridgecloud.sharepoint.com/sites/AD_ExamOperationsandMitigatingCircumstances.

[2] Includes Preliminary, Qualifying and Honours Examinations, examinations requiring external accreditation, and re‑sits.

(b) By revising the Ordinance for Entries and Lists of Candidates for Examinations (Statutes and Ordinances, p. 256) to read as follows:

1. No candidate may be entered for any examination after the latest date specified in the Table of Dates for the submission of entries; nor shall any alteration of an entry in the list of candidates, other than the withdrawal of a candidate or of an entry, be permitted after that date.

2. Any entry of a candidate who proposes to offer less than is required by the regulations for the examination concerned shall require the approval of the General Board. The name of any such candidate shall not be included in the class-list for that examination.

3. In accordance with regulations made from time to time by the General Board governing postgraduate degrees and other qualifications,[1] the Examiners for any taught course shall have power at the request of a Degree Committee to arrange for the examination of postgraduate students and to report their results to the Secretary of the Degree Committee. The names of such students shall not appear in any class-list.

4. Notwithstanding the above regulations or the Ordinance for Setting the Table of Dates for Examinations, the General Board may accept a list of candidates or a class-list or a list of candidates approved for a degree or other award later than the latest day or time prescribed, if the General Board considers it necessary to take this action to protect the interests of students and is satisfied that academic standards will be maintained.

[1] See the General Regulations for Certain Postgraduate Degrees and Other Qualifications, p. [435].

(c) By replacing the Ordinance for Dates of Examinations (Statutes and Ordinances, p. 259) with the following new Ordinance:

1. In September of each year the General Board shall announce a Table of Dates in consultation with the Faculty Boards or comparable authorities concerned giving the earliest date of the examinations to be held in the following academic year and the dates by which entries of candidates and corrections of those entries are to be submitted to the Registrary. The General Board shall determine the information to be provided and the manner in which that information is to be provided.

2. The latest dates for providing to the Registrary, where applicable, the approved class‑lists of examinations for all taught courses shall be as follows:

The Monday before the days of General Admission:

The class-lists for undivided Triposes, Part II examinations for Triposes, Part IIa of the Chemical Engineering Tripos, Part Ib of the Medical Sciences and Veterinary Sciences Triposes, Part Ib of the Natural Sciences Tripos, Part IIa of the Manufacturing Engineering Tripos, and the Second Examination for the B.Th. Degree.

The Friday after the days of General Admission:

The class-lists for all other Honours Examinations, for the LL.M. Examination and the Mus.B. Examination, for the Preliminary Examinations, Qualifying Examinations, Certificate Examinations, and the First Examination for the B.Th. Degree.

3. Each Chair of Examiners shall send to the Registrary by the date specified in the Table of Dates a list of such examinations as require one or more Examiners to be present in person at the start of the examination.

4. Notwithstanding the above regulations, the General Board may start any examination later than as prescribed, if the General Board considers it necessary to take this action to protect the interests of students and is satisfied that academic standards will be maintained.

(d) By revising paragraph (a) of the Ordinance for Assessment Formats (Statutes and Ordinances, p. 262) to read as follows:

(a)In‑person invigilated handwritten examinations

(e) By revising the Ordinance for Interviews (Statutes and Ordinances, p. 262) to read as follows:

Notwithstanding the provisions of any other Ordinance, the Examiners for any taught course shall have discretion to summon any candidate for an interview on any aspect of the work submitted.

(f) By retitling the Ordinance for the Approval of Class-lists (Statutes and Ordinances, p. 263) as the Ordinance for Examination Meeting Attendance and the Approval of Class-lists, and by amending paragraphs (a) and (b) of Regulation 1 to read as follows:

(a)for any Part of the Medical Sciences Tripos or the Veterinary Sciences Tripos, or for Part Ia or Part Ib of the Natural Sciences Tripos, the meeting of the Examiners at which the marks of the candidates in their particular subject are finally approved;

(b)for any other examination for which a class‑list is published, the meeting of the Examiners at which that list is finally approved.

(g) By replacing the General Regulations for Examiners and Assessors (Statutes and Ordinances, p. 264) with the following new Ordinance:

1. The Faculty Board or comparable authority shall appoint Examiners and Assessors for all taught courses.

2. The General Board shall appoint, on the nomination of the Faculty Board or comparable authority, for each taught course a resident member of the Regent House as Chair of Examiners for each board of Examiners and where required, a Senior Examiner and/or External Examiners.

3. The General Board shall announce the dates by which all appointments under this Ordinance shall normally have been made. If necessary, appointments may be made after the normal date subject to the approval of the General Board.

(h) By rescinding the following Ordinances:1

Disclosure of Examination Marks (Statutes and Ordinances, p. 263)

Payments to Examiners, Assessors and Supervisors (Statutes and Ordinances, p. 265)

1The following Ordinances are retained in Chapter III without amendment; Honours Examinations; Allowances to Candidates for Examinations (see separate Report proposing changes, Reporter, 6784, 2024–25, p. 560); and Marking and Classing Conventions and Criteria.

If the changes in Annex A are approved, the General Board has agreed to make the following changes to General Board Regulations from the same date.

(a) In the regulations for the following degrees, by deleting the listed regulations or parts of regulations concerning the Faculty Board or Degree Committee nominating Examiners and Assessors, renumbering the remaining regulations and updating any cross-references:

Master of Accounting (Statutes and Ordinances, p. 437): Regulation 7.

Master of Business Administration (Statutes and Ordinances, p. 441): Regulation 7.

Master of the Conservation of Easel Paintings (Statutes and Ordinances, p. 445): Regulation 6.

Bachelor of Theology for Ministry (Statutes and Ordinances, p. 447): Regulation 8.

Master of Education (Statutes and Ordinances, p. 452): Regulation 7.

Master of Finance (Statutes and Ordinances, p. 458): Regulation 8.

Master of Corporate Law (Statutes and Ordinances, p. 459): Regulation 11.

Bachelor of Music (Statutes and Ordinances, p. 484): Regulation 9.

Master of Music (Statutes and Ordinances, p. 485): Regulation 10.

Advanced Diploma in Economics (Statutes and Ordinances, p. 573): First sentence of Regulation 8.

Advanced Diploma in Hebrew Studies (Statutes and Ordinances, p. 574): Regulation 5.

Postgraduate Diploma in Legal Studies and Postgraduate Diploma in International Law (Statutes and Ordinances, p. 575): First sentence of Regulation 7.

Advanced Diploma in Research Theory and Practice in English (Business Management) (Statutes and Ordinances, p. 576): Regulation 4.

Advanced Diploma in Theology, Religion, and Philosophy of Religion (Statutes and Ordinances, p. 576): Regulation 4.

General Regulations for Certificates of Postgraduate Study (Statutes and Ordinances, p. 578): Regulation 9.

Postgraduate Certificate in Education (Statutes and Ordinances, p. 585): Regulation 6.

(b) By making the following amendments:

Master of Law (Statutes and Ordinances, p. 460), Regulation 13: By amending the first clause to read ‘Examiners for the LL.M. Examination shall be appointed by the Faculty Board of Law;’.

Bachelor of Medicine and Bachelor of Surgery (Statutes and Ordinances, p. 465), Regulation 24: In paragraphs (a ) and (b) by replacing the phrase ‘the Faculty Board shall nominate’ with ‘the Faculty Board shall appoint’.

Doctor of Medicine (Statutes and Ordinances, p. 472), Regulations 4 and 5: By replacing the references to appointments made by the General Board on the nomination of the Faculty Board of Clinical Medicine with references to appointments made by the Faculty Board of Clinical Medicine.

Master of Philosophy by Advanced Study (Statutes and Ordinances, p. 498), Regulation 15: In the first sentence by replacing the phrase ‘The Degree Committee concerned shall nominate for appointment by the General Board’ with the phrase ‘The Degree Committee concerned shall nominate for appointment by the Faculty Board’.

Bachelor of Veterinary Medicine (Statutes and Ordinances, p. 561), Regulations 18(b) and 19: By replacing references to appointments made by the General Board on the nomination of the Faculty Board of Veterinary Medicine with references to appointments made by the Faculty Board of Veterinary Medicine.

(c) In the General Regulations for the Constitution of the Faculty Boards (Statutes and Ordinances, p. 601), by revising Regulation 6 to read as follows:

6. Each Faculty Board shall appoint such examiners and assessors, and submit to the General Board nominations of such examiners, as required by Ordinance or General Board Regulations.

The Council begs leave to report to the University as follows:

1. The Council is required to make an annual Report to the Regent House recommending allocations from the Chest to Schools, institutions and centrally administered funds. Chest allocations and associated Chest expenditure cover the majority of the recurrent pay costs of the University’s academic and professional services posts; however, Chest financial information excludes all research activity, some teaching activity and some other activities.1

2. The University currently forecasts using two different approaches; a bottom-up, Chest-focused planning process linked to available funding sources, and a top-down, overall cash flow model (known as the Ten-Year Model) built from most recent actual results. Enhanced Financial Transparency (EFT), once the new finance system has been brought in, will align bottom-up and top-down planning, meaning institutions can plan on an EFT basis and strategic modelling (at the level of the Finance Committee) can be transparently reconciled to the bottom‑up approach. However, until the new finance system is brought in, most institutions continue to rely on planning that is focused on the Chest.2

3. The Finance Committee has agreed a roadmap for the Finance Transformation Programme (FTP), including the replacement of the University Finance System (CUFS) and a new chart of accounts that, together, enable achievement of EFT’s goal to provide reliable and transparent financial information that empowers institutions to make better informed decisions and to plan and budget in generally accepted, straightforward, and efficient ways.

4. In the meantime, Schools and Non-School Institutions (NSIs) continue to be resourced, in part, via Chest allocations, with the Council continuing to make an annual Report recommending allocations from the Chest to Schools, NSIs and centrally administered funds. This Chest allocations Report is made in the context of both the total Academic University position and the financial outlook of the University Group (including Cambridge University Press & Assessment).

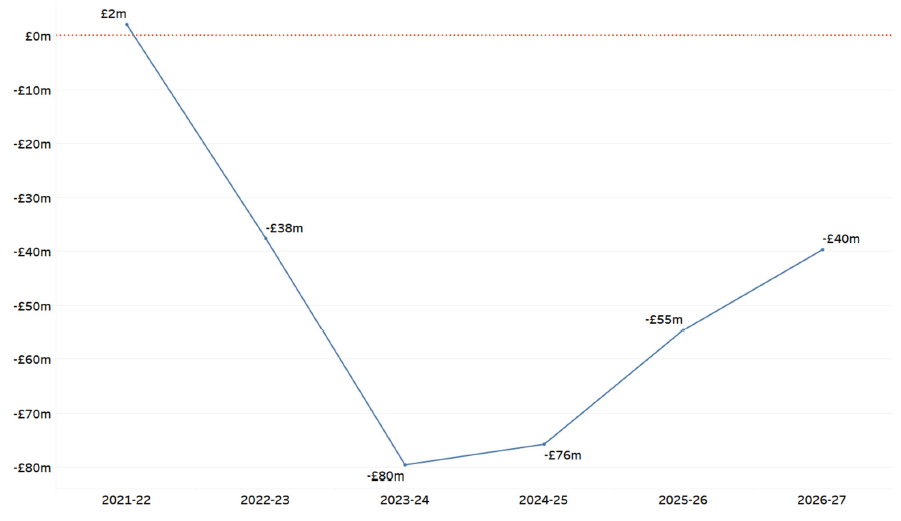

5. The University Group as a whole (including Press & Assessment) generates an annual cash flow surplus from its operations and distributions from the endowment. As has been the case for the past several financial years, however, the proposed 2025–26 Budget for the Academic University is a concern. The overall operating cash flow position for the Academic University as reported to the Finance Committee in October 2024 was an overall deficit of £59.5m in 2023–24. A similar deficit is projected for 2024–25 (a deterioration relative to a projection of £47m on a like‑for-like basis for 2024–25 at this time last year). On this basis, a deficit of £40–45m is predicted for 2025–26.

6. Staff numbers have continued to increase and this has added to the costs arising from National Insurance changes with effect from April 2025. The reduction in energy prices expected in last year’s Report has been delayed. Other operating costs are, overall, increasing materially more than inflation. Projected income from the CUEF, donations and restricted grants remain insufficient to close the gap between core operating income and expenditure.

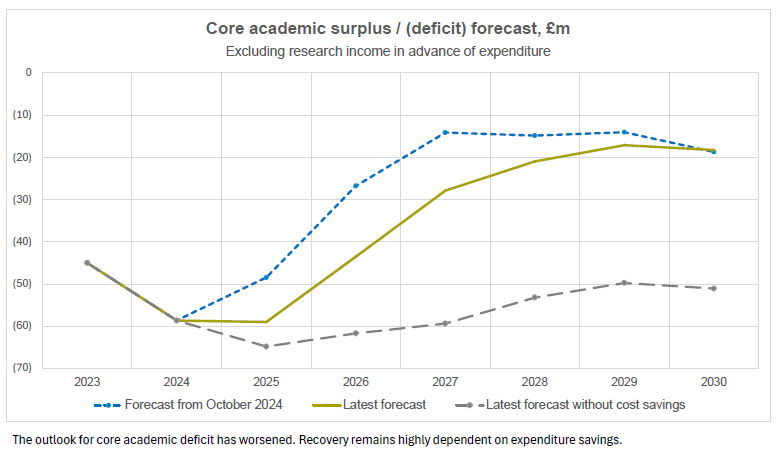

7. The projections in the latest version of the Ten-Year Model suggest that even with an assumed 5% reduction in expenditure – as endorsed by the Council and the General Board in 2024 – the deficit for the Academic University will remain within a range of £20m to £40m for the foreseeable future. The same trajectory is indicated by the EFT prototype, as illustrated more fully in Annex 3 to this Report.

8. Recent Allocations Reports have emphasised that the ambition of a sustainable annual cash flow surplus from core academic operations is only achievable in the medium term if appropriate revenue growth is secured, costs kept under control and cost saving programmes which do not reduce the academic potential of the University delivered. Cash flow deficits from core academic operations must be met from unrestricted reserves, while a failure to deliver a cash surplus from core academic operations leaves the University substantially reliant on Press & Assessment and philanthropy for the capital it needs for investment to remain a world leading university.

9. Subsequent to last year’s Report, several University‑wide transformation programmes have made progress in defining their contribution towards the University’s financial sustainability:

•The Reshaping our Estate programme has developed a Strategic Estate Framework and Capital Plan which the Estates Committee has now recommended to the General Board and the Council. As well as achieving very substantial improvements to the overall quality of the University estate, the Framework and Plan are expected to reduce the size of the estate by 10% over the next twenty years. This will reduce annual running costs by c. 10% against the current level and c. 25% set against a counterfactual ‘continue as is’ model (in today’s money).

•Subject to Regent House approval, the first substantial project to be implemented will be the disposal to King’s College of the site and buildings on the north side of Mill Lane.

•In addition, the School of Clinical Medicine is working with the Estates Division to rationalise its use of space on the Biomedical Campus, with the ambition of withdrawing altogether from one building in 2026.

•The Finance Transformation Programme completed its procurement process and selected a systems integration partner in December 2024; a business case to complete FTP was approved by the Planning and Resources Committee (PRC) in March 2025. FTP has completed a robust scrutiny process including external validation of its readiness to proceed, and a contract with the SI partner has been signed with a target date for the new finance system to ‘go live’ in May 2027. The scope of the programme includes significant opportunities for both tangible and intangible financial benefits. A current example is invoice automation, which is being rolled out across the Academic University and is expected to enable both efficiencies and improved purchasing data.

•Transforming Research Support (TRS) has implemented a new grants management platform, and has received approval from the PRC to proceed with a second and final phase of the programme that will transform the operating model for research support, with measurable benefits that are expected to include substantial operational savings through improved efficiency, and increased grant income in areas where externally funded research is currently constrained by administrative capacity.

10. Last year’s Report recognised that the savings potential of the transformation programmes cannot be realised immediately, and that more immediate steps are required to reduce the scale of the operating deficit. The Council and the General Board endorsed a 5% reduction in overall operating expenditure (Chest and non‑Chest), and the PRC, at a joint meeting with the Finance Committee in May 2024, agreed that a 5% reduction in Chest expenditure would be implemented through a reduction in Chest allocations of 5% for all institutions across 2024–25 and 2025–26 financial years.

11. The PRC has encouraged Schools and institutions to control and reduce expenditure across their entire range of activities, where this will not unduly undermine academic activity or frustrate plans to generate sustainable, additional income. There is, however, no recent precedent for the central University to impose controls on non-Chest expenditure.

12. The PRC has agreed two principal mechanisms for encouraging non-Chest savings, commencing in 2025–26 and expected to continue until EFT is brought in. One is a 5% overhead to be levied on external trading and Gift Aid3 income, applied to departments with external trading income exceeding £500k p.a. The other is a similar levy on the departmental share of research overheads, to be applied to the departmental share after the usual income allocation policy has been applied to each research grant.4 The forecast income collected as consequence of these measures is reflected below as an increase in forecast Chest income.

13. Until the new finance system, with its new chart of accounts, is brought in, Schools and NSIs are partially resourced via Chest allocations. A practical mechanism to drive achievement of the overall reduction in expenditure endorsed by the Council and the General Board is, therefore, a reduction in Chest allocations. Chest allocations to Schools, non-School institutions and centrally administered funds have accordingly been reduced by 5% in real terms5 across the 2024–25 and 2025–26 financial years.

14. Chest allocations are determined by a Chest allocations framework which agrees a baseline and applies an inflation rate aligned to the assumptions for pay and non-pay inflation that drive the Ten-Year Model.6 The effective rate of inflation on Chest allocations in 2025–26 is 3% for staff costs and 2.2% for non-staff costs (2025–26) and 3% for staff costs and 1.8% for non-staff costs (2026–27).

15. As a first step towards the 5% reduction in Chest allocations and expenditure that are required by the end of 2025–26, allocations to Schools and NSIs in 2024–25 were reduced, after inflation (including pay inflation) has been applied, by an initial 1%. Chest allocations for 2025–26 have therefore been reduced by a further 4%, again after inflation (including pay inflation) has been applied.

16. The following paragraphs summarise the current forecast position of the Chest for 2024–25 and 2025–26.

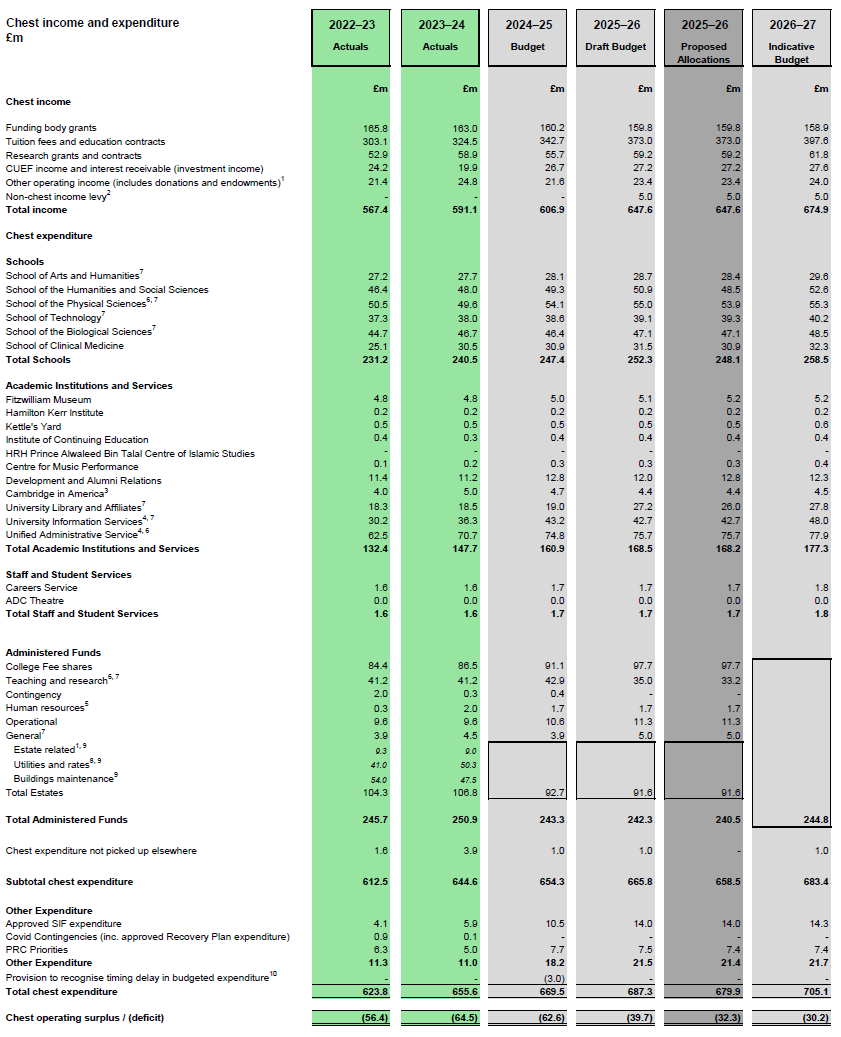

17. Chest income in 2024–25 was budgeted at £606.9m, with the 2024–25 in-year forecast now indicating that income at £608.7m. The University’s recurrent research funding from Research England reduced by approximately £0.5m in 2024–25, reflecting revised calculations of QR funding for business-funded and charity-funded research; this is, however, approximately £1m higher than the previous forecast for 2024–25.

18. The principal increase to budgeted Chest income in 2025–26 is an increase in tuition fee income of £30.3m (Chest tuition fee income only, compared to Chest tuition fees in the 2024–25 Report). This is driven by greater predicted numbers of Masters-level taught postgraduate students and increases in unregulated fees.

19. The University’s recurrent funding from Research England and the Office for Students is assumed to be unaltered in 2025–26, pending receipt of grant letters from both organisations in due course.

20. The additional Chest income attributable to the mechanisms for encouraging non-Chest savings, as summarised in paragraph 12 above, is budgeted at approximately £5m.

21. Chest allocations for 2025–26 have been reduced by a further 4%, after inflation (including pay inflation) has been applied.7 The immediate implications for overall operating expenditure in 2025–26 are expected to vary across the University.

•For the UAS and most centrally administered funds – which have limited cash reserves – the reduction in Chest allocations is expected to translate directly into reduced expenditure. A material exception is Cambridge Enterprise, which will reduce overall expenditure by 5% but nonetheless requires a higher Chest allocation in 2025–26 towards a funding shortfall that has resulted from lower equity realisations.

•In Schools and some NSIs, a balance has been struck in the short-term between genuine reductions in expenditure (e.g. from strategic funds managed at School level), and use of reserves to fund activity that would otherwise have been funded from the Chest, pending the further development and implementation of plans to achieve sustainable reductions in expenditure, and materially increase income,8 in 2026–27 and subsequent years.

•The financial plans prepared by University Information Services (UIS) indicate that reserves will be fully committed to fund expenditure in 2025–26, without yet a firm plan to reduce expenditure in 2026–27. A new Chief Information Officer joined the University in April 2025 and will convene a discussion with Schools and institutions that will inform firm proposals for the delivery of information services across the University on a basis that is financially sustainable.

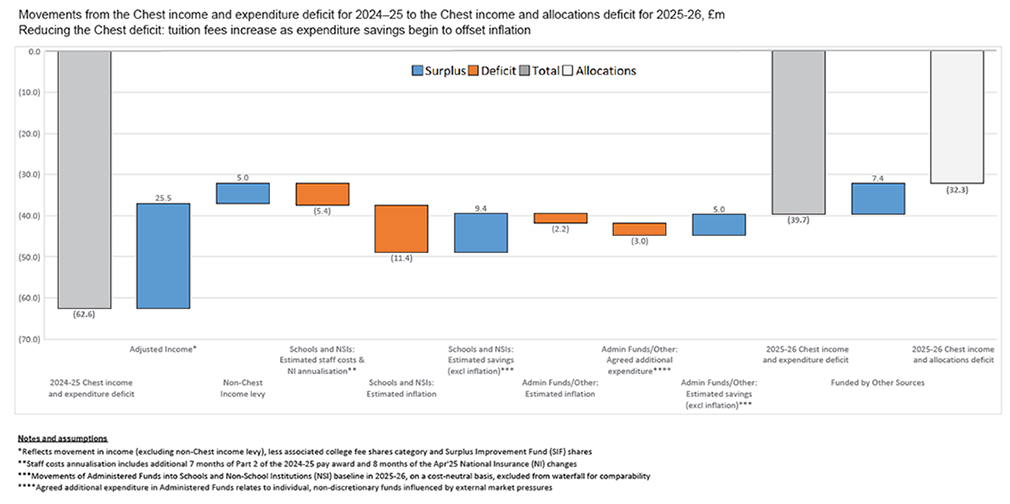

22. Overall, the combined effect of a budgeted increase in Chest fee income and the expected reductions in Chest expenditure resulting from the reduction in Chest allocations is a projected Chest expenditure deficit in 2025–26 of £39.7m. The Chest expenditure deficit translates to a Chest allocations deficit (Chest income less Chest allocations) of £32.3m. The impact is summarised in Annex 2 below.

23. The University Group as a whole (including Cambridge University Press & Assessment) continues to generate an annual cash surplus from its operations and distributions from the endowment. The Group’s balance sheet remains strong.

24. Nonetheless, the cost base of the Academic University remains high. Cash flow deficits from core academic operations must be met from unrestricted reserves, while a failure to deliver a cash surplus from core academic operations leaves the University substantially reliant on Press & Assessment and philanthropy for the capital it needs for investment to remain a world leading university.

25. The ambition of a sustainable annual cash flow surplus from core academic operations, sufficient to provide the surplus headroom required for long-term renewal and academic investment is only achievable in the medium term if costs are kept under control and planned cost saving programmes, which do not reduce the academic potential of the University, are – in due course – delivered to the bottom line. The University-wide transformation programmes continue to offer the best opportunity to capture significant levels of efficiencies in the medium term.

26. The requirement for Schools and institutions to achieve by the end of 2025–26 – and to sustain into 2026–27 and subsequent years – 5% reductions in overall operating expenditure (Chest and non-Chest) is unaltered. As indicated in last year’s Report, this will be achieved in part by a further reduction of Chest allocations to Schools and institutions in 2025–26.

27. Taken in the context of both the University Group and the Academic University’s overall financial position, the Council recommends:

I.That allocations from the Chest for the year 2025–26 be as follows:

(a)to the Council for all purposes other than the University Education Fund: £215.2m.

(b)to the General Board for the University Education Fund: £464.7m.

II.That any supplementary grants from the Office for Students and UK Research & Innovation (through Research England), which may be received for special purposes during 2025–26, be allocated by the Council, wholly or in part, either to the General Board for the University Education Fund or to any other purpose consistent with any specification made by the OfS or UKRI, and that the amounts contained in Recommendation I above be adjusted accordingly.

Annex 1: Chest income and expenditure, including recommended Chest allocations for 2025–26 (p. 614).

Annex 2: Comparison between Chest income and expenditure deficit, and Chest income and allocations deficits, 2024–25 and 2025–26 (p. 616).

Annex 3: Enhanced Financial Transparency – financial information for the Academic University (p. 617).

Annex 4: University business information (student numbers by level of study and fee status, non-regulated fee rates, staff numbers by academic employment function, research performance) (p. 620).

Deborah Prentice, Vice-Chancellor

Sarah Anderson

William Astle

Gaenor Bagley

Milly Bodfish

Daniela De Angelis

John Dix

Sharon Flood

Alex Halliday

Heather Hancock

Simon McDonald

Ella McPherson

Scott Mandelbrote

Ewa Marek

Sally Morgan

Mezna Qato

Jason Scott-Warren

Alan Short

Pieter van Houten

Andrew Wathey

Garth Wells

1Chest income comprises unrestricted general income to the University principally from Research England and the Office for Students, student fees and endowment income, and a share of the ‘overhead’ element from research grant income, which is brought into the Chest to offset costs incurred in support of research. Non-Chest income consists principally of research grants, trust funds and other restricted funds, specific donations and trading activity carried out by departments and institutions. It is, for the most part, received and managed directly by relevant local institutions.

2The Council reported to the Regent House in 2022 on the transition to EFT. Preliminary changes to the University’s Statutes have been made which support the ongoing oversight of the University’s budget by the Regent House. The Regent House is reminded that these changes do not commit the University to the adoption of EFT or the removal of the Chest as a central part of the University’s financial structures, which would need to be approved by separate Grace(s).

3Gift Aid sources of funds which are specifically related to gift aid associated with external trading, for example subsidiaries such as Judge Business School Executive Education Limited (JBSEEL).

4A 5% levy on the departmental share of research overheads will result in a revised share; for example 81% Chest : 19% department for all sponsors other than Industry.

5After allowing for inflation.

6Inflation rates from the Ten-Year Model October 2024 update have been used for the Chest budget for 2025–26, as recent Ten-Year Model inflation assumptions are not materially different to October 2024.

7For those institutions and activities – principally the UIS and the centrally administered funds – for which no reduction in Chest allocation was applied in 2024–25, the full 5% reduction has been applied in 2025–26.

8For example, the School of the Humanities and Social Sciences has firm plans to increase non-regulated fees in 2026–27 that may increase Chest income, beyond what is currently assumed in this Report, by approximately £2m.

1From 2024–25, the income received from Cambridge University Press and Assessment (CUPA) in respect of capital equipment fund allocations to Schools is routed to/from the investment fund (to match expenditure), not via the Chest.

2From 1 August 2025, until EFT is brought in, a 5% levy will be imposed on: external trading activity and associated gift aid (applied to departments on income above £500k), and the departmental share of research overheads, as a means of encouraging savings on non-Chest activity. An estimate for the potential income generated has been included in the draft and indicative figures for 2025–26 and 2026–27 above, similar to the current mechanism for Indirect Cost Charge (ICC) overheads.

3The Chest absorbs the impact of foreign exchange transactions in relation to the Cambridge in America allocation.

4Chest expenditure (and allocations) excludes change and transformation programmes funded from the Investment Fund.

5Since 2024–25, in-year costs of individual promotion schemes are no longer associated with the Administered Funds, but instead provided through the pay inflation, which includes promotion costs, applied to Schools and NSIs.

6In 2024–25, transfers were made from Administered Funds to Schools. The PRC approved the transfer of Cambridge Zero funds to the School of the Physical Sciences, with an additional allocation of £0.52m. All other transfers were cost-neutral, Widening Participation funds were transferred to UAS, and Researcher Development Funds were transferred to Schools and UAS.

7In 2025–26, several transfers from Administered Funds into Schools and NSI baselines will take place, all on a cost-neutral basis. These include the transfer of Year Abroad funds to the School of Arts and Humanities, funds allocated towards specific M.Phil. course costs to the School of the Biological Sciences, the School of the Physical Sciences, and the School of Technology, the Journal Coordination Scheme to the University Library, and the Technology Development Fund to UIS.

8From 2025–26, utilities and rates includes a £1.2m allocation in respect of the University’s use of space at the CUPA site on Shaftesbury Road.

9Estates Division continue to review expenditure plans at a total portfolio, as indicated by the boxed rows, in order to prioritise expenditure.

10Since 2022–23 budget, a provision has been made to account for the timing difference between budgeted expenditure and when expenditure is actually incurred. This provision has been reduced to £0.0m between 2022–23 and 2025–26, firstly due to the effect of a Chest allocations holdback mechanism which applied to the years 2022–23 and 2023–24, and secondly due to the savings targets which are applied to the years 2024–25 and 2025–26. These mechanisms all had/have the effect of bringing actual expenditure closer to budget.

1. The University continues to develop its new approach to planning and budgeting as part of the EFT project within the Finance Transformation Programme (FTP).

2. EFT’s goal is to provide reliable and transparent financial information so that institutions are empowered to make better informed decisions and to plan and budget in generally accepted, straightforward, and efficient ways. Through EFT, income will be attributed where earned, costs aligned to those income streams where incurred, and indirect costs such as libraries or the research operations office attributed according to a fair and equitable set of drivers1. Regardless of whether institutions operate in surplus or deficit, it is hoped that EFT will lead to improvements in financial outcomes and contribute to an improvement in overall financial sustainability.

3. A new Chart of Accounts, together with a planning module within the new finance system and new financial policies and regulations, are required to implement EFT in full. These are anticipated in spring 2027, alongside the planned change in the finance system. During the transition to EFT, preliminary financial information is available via a prototype income and expenditure model which maps real financial data from CUFS2. This prototype has been shared with leadership teams in Schools and non-School institutions for the past three years. The prototype should not be considered a proxy for full EFT functionality.

4. The EFT prototype’s forecasts for 2024–25 and subsequent years are built on the 2023–24 actuals. Income includes updated information for student numbers and fee rates for 2025–26 and 2026–27 and the latest insights into the mix and volume of research grants and contracts. Expenditure includes the latest assumptions for staff costs and non-staff costs inflation.

5. Enhancements have been made to the EFT prototype within the last 12 months, including:

•A split of the prototype data by current classifications of unrestricted and restricted funding sources

•Improved granularity of Tableau dashboards which allow users to drill down to department level for income and expenditure, and activity-level reports. As improved data presentation is delivered consideration will be made as to how sensitive data will be shared.

High-level graphical information from the EFT prototype is shown below, with full details being made available to Schools and institutions from June 2025.

|

Academic University £m |

Actuals Years |

Plan Years |

||||

|

2021–22 |

2022–23 |

2023–24 |

2024–25 |

2025–26 |

2026–27 |

|

|

Tuition fees and education contracts |

362.490 |

372.740 |

394.934 |

407.679 |

445.628 |

472.937 |

|

Total funding body grants |

177.416 |

181.647 |

179.829 |

176.181 |

175.234 |

175.514 |

|

Research grants and contracts |

517.630 |

532.152 |

552.180 |

551.904 |

592.469 |

618.004 |

|

Other income |

197.315 |

220.510 |

226.799 |

235.154 |

244.284 |

252.435 |

|

Donations and endowments |

29.553 |

48.361 |

46.140 |

47.714 |

49.265 |

50.555 |

|

Investment income |

63.230 |

75.990 |

84.227 |

86.686 |

89.257 |

91.879 |

|

Total income |

1,347.634 |

1,431.401 |

1,484.110 |

1,505.317 |

1,596.136 |

1,661.325 |

|

Staff costs |

713.036 |

749.269 |

777.902 |

791.025 |

823.754 |

844.403 |

|

Other operating expenses |

632.510 |

719.749 |

785.504 |

790.065 |

827.009 |

856.601 |

|

Attribution Above Contribution Line |

0.000 |

0.000 |

0.000 |

0.000 |

0.000 |

0.000 |

|

Total Expenditure |

1,345.546 |

1,469.018 |

1,563.406 |

1,581.090 |

1,650.763 |

1,701.005 |

|

University surplus/deficit |

2.088 |

-37.616 |

-79.596 |

-75.773 |

-54.627 |

-39.679 |

1. The model currently extrapolates from a single year’s data. Due to postings in the current chart of accounts which are based on resource allocation accounting, actuals may include distorting anomalies which could potentially distort forecast years: the prototype cannot readily handle one-off anomalies.

2. Treatment of certain income and expenditure lines differs between the Ten-Year Model and the EFT prototype, including presentation of the Investment Fund. Work continues on the new Chart of Accounts to understand how these differences occur, in order to build transparent reporting when the new finance system goes live.

3. Improvements have been made to the handling of shared Triposes in the Plan years (i.e. 2024–25 onwards). In addition, further adjustments have been made to consistently reflect the split of the UG for Medicine course between the School of the Biological Sciences and the School of Clinical Medicine in past and future years.

4. Two Schools are in surplus both before and after deduction of their share of central costs, with the other four showing surpluses at the gross contribution level but deficits at the net contribution level.

5. The figures for the Schools have remained relatively stable; however, ongoing work is required to improve internal accounting adjustments required for the Group accounts, which can impact some central CUFS departments including the centrally administered funds. An EFT/Chart of Accounts workstream is reviewing transactions and processes with a view to identifying transactions relevant to academic departments and NSIs where appropriate, and where Group activity needs to be more clearly ring-fenced and excluded from the financial transactions of the Operational Academic University.

The EFT prototype has been shared with Schools and institutions, at or around the date of the May PRC meeting in 2023 and 2024, and the updated information will again be shared with institutions in detail following the May 2025 PRC meeting. Each year the prototype has provided valuable information to inform the development of EFT principles and requirements.

Work to deliver EFT is ongoing within FTP workstreams including:

(a)Development of detailed Chart of Account solutions to deliver EFT requirements

(b)Development of technical accounting plans to move from Chest accounting to income and expenditure accounting

(c)Development of planning and project budgeting systems to deliver improved financial planning, budgeting, forecasting and reporting solutions

(d)Ongoing work in governance and policy areas to support successful deliver of EFT objectives

(e)Continued development of detailed worked examples, including use of prototype data to examine pilot financial planning issues

(f)Ongoing stakeholder change and communications engagement to support understanding of the detailed changes from EFT and FTP

EFT draft principles were shared with the PRC and Finance Committee at a workshop in October 2024, together with worked examples to demonstrate how the principles may operate in practice. Material from this workshop was subsequently taken around the University in Lent and Easter Term 2025, in the form of a roadshow. This roadshow visited all six Schools and held two sessions for non-School institutions, inviting more than 450 colleagues to attend. A further virtual session was held for Finance Division colleagues, from which a recording will be made available to stakeholders across the University. The presentation was led by Professor Anna Philpott (PVC Resources & Operations) and delivered by the EFT team.

The key themes that were discussed at the roadshow were:

•Contributions and incentives for Schools and public-facing institutions

•Contributions and incentives for enabling institutions such as the UAS

•Dealing with lumpy income and expenditure

•Attributing indirect costs

•Financial transparency

The overall response was resoundingly positive with colleagues appreciating the chance to ask questions and discuss details to test their understanding and reinforce knowledge. 95% of attendees said they found the roadshow informative and 92% said it was a good use of their time. More importantly, 100% said they understood why we need EFT, and 97% believed it is the right thing for the University. Feedback and questions have been collated in order to help shape the future direction of EFT and produce Frequently Asked Questions that staff can refer to.

The EFT team, which includes School and non-School Finance Business Partners, are currently planning the next EFT change and engagement sessions. This will include the roll out of 2025’s updated EFT prototype to demonstrate how EFT financial information may look to Schools, departments and institutions with their prototype data.

1A driver is an agreed method to share central income or costs, for example sharing the costs of the HR Division by staff numbers, or space costs per m2. Once central costs have been shared out these are described as indirect costs.

2Cambridge University Finance System (CUFS) is structured around Chest and non-Chest financial information. EFT will remove the distinction between Chest and non-Chest, and the prototype looks through Chest and non-Chest barriers to report on the totality of the Operational Academic University.

Business information is shared with University committees to provide a University-wide picture of the size and shape of our activities, and to broaden the understanding of our levers to financial sustainability.

The information is available on the University’s Tableau server: https://tableau.blue.cam.ac.uk/#/site/InformationHub/projects/427 (CRSid and UIS password required). Each dashboard contains a notes section that explains the sources of the data, main definitions and any contextual detail that needs to be taken into account when considering the numbers.

The following dashboards are available:

This dashboard provides a time series presenting the changes in the size and shape of the University’s student population. It presents an overview of student numbers by both total student population and new entrants and offers, at a glance, a view of the main trends such as a growth in PGT Masters and a gradual change in the balance of Home/International students across all levels of study. The latter is partially related to the change of fee status for EU students post-Brexit. A more detailed report is available by School. It further includes comparison with the student number trends at the University of Oxford and other Russell Group universities.

This report shows the range of non-regulated fee rates by School. It illustrates patterns of clusters and outlier rates and can support Schools in their consideration of setting any course-specific rates. It provides data on all rates side by side to encourage decisions towards greater alignment of fees and the banding of the fee rates wherever possible. There is also a comparator of the average fee rates by level of study with the main competitor institutions.

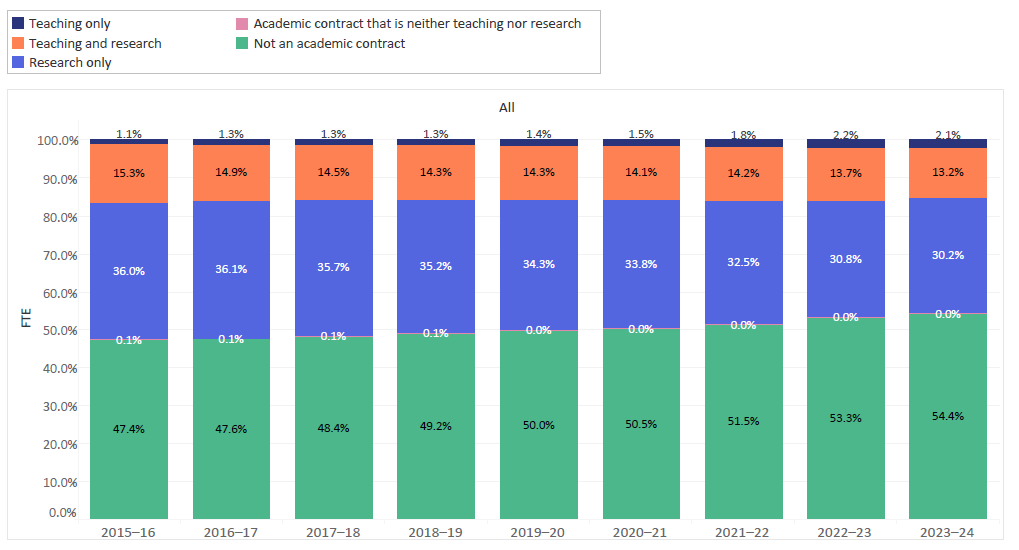

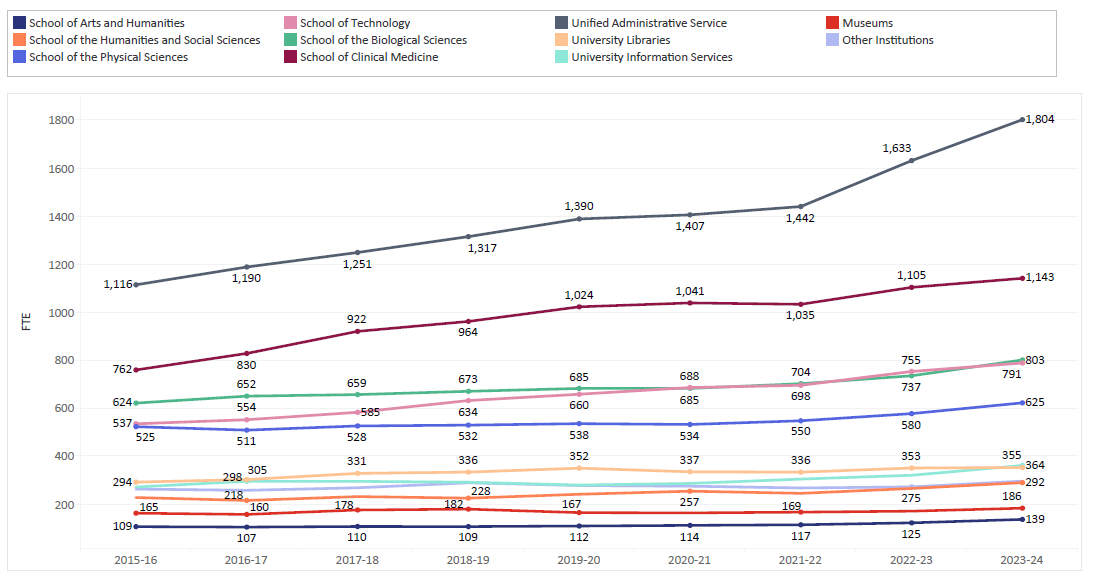

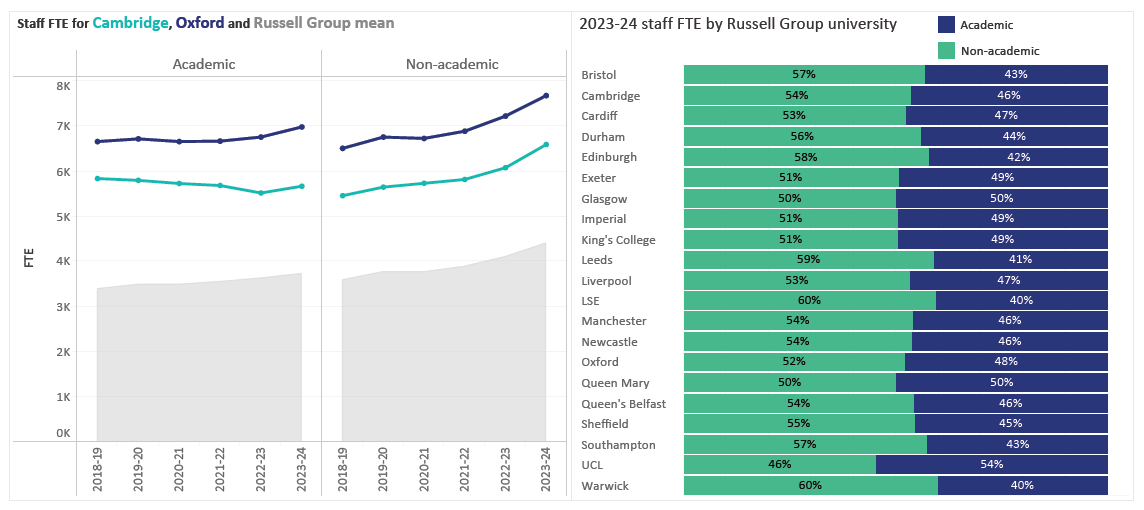

This dashboard provides a view of changing staff numbers across university institutions. It provides information on institution, headcount, full-time equivalent (FTE), and employment function to deliver a snapshot of staffing patterns. It also contains benchmarking information with Russell Group universities by employment function.

The charts on pages 621–624 show staff FTE data up to the 2023–24 academic year.

This dashboard examines the trends in the income in respect of externally sponsored research at the University of Cambridge and other Russell Group universities, based on the data submitted to the Office for Students (OfS) as the Annual Financial Return (AFR). It should be noted that AFR guidance specifies that research income should include capital grants for the purpose of research (such as grants for land, buildings or equipment used for research and the refurbishment of research facilities) except for capital grants from Research England. The University of Cambridge received a substantial capital grant for the Ray Dolby Centre, which is included in the research income numbers in years 2018–19 and 2019–20 under the Research Councils funder category and Physics (114) HESA cost centre.

E. M. C. RAMPTON, Registrary

END OF THE OFFICIAL PART OF THE ‘REPORTER’